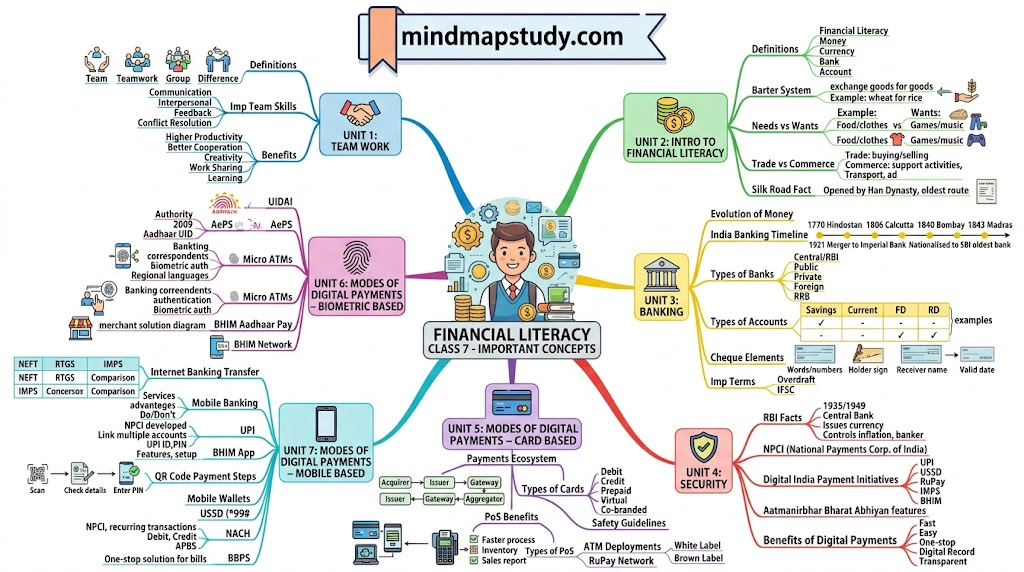

Financial Literacy Class 7 is skill education course to understanding money, banking, and digital payments through seven clear units.This post covers seven units of financial literacy for Class 7 — from teamwork and basic money concepts to digital payments and biometric banking.

Table of Contents

| Unit | Topic | Page |

|---|---|---|

| 1 | Team Work | 4 |

| 2 | Introduction to Financial Literacy | 8 |

| 3 | Banking | 14 |

| 4 | Security | 24 |

| 5 | Modes of Digital Payments – Card Based | 33 |

| 6 | Modes of Digital Payments – Biometric Based | 45 |

| 7 | Modes of Digital Payments – Mobile Based Banking and Others | 51 |

Unit 1: Team Work

1. Teamwork

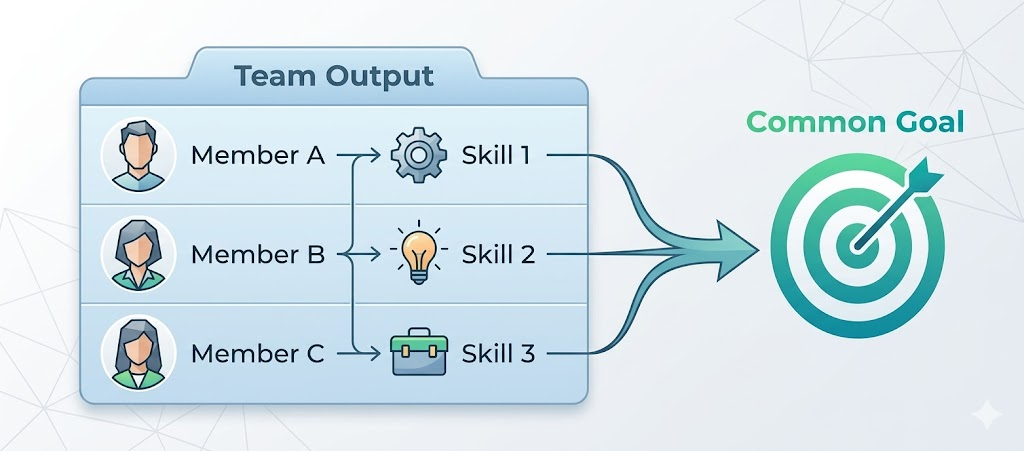

A team is a group of people who come together to perform a common goal or objective. Common examples are a football team, cricket team, or tug-of-war team. In business organisations, these are called work teams.

When members of a team perform some work together, it is called teamwork. Effective teams make challenging tasks achievable and straightforward because each member contributes based on their unique abilities and skills.

A cricket team is a good example — the coach and players choose a captain, wicket-keeper, batsmen, all-rounders, and bowlers. Each person’s role is different, but the purpose — winning — is the same.

1.1 Effective Team Skills

For a team to work well, every member needs to demonstrate specific skills:

| Skill | What It Means |

|---|---|

| Communication Skills | Listen attentively and put across thoughts clearly |

| Interpersonal Skills | Build harmony and cooperation within the team |

| Feedback Skills | Give and receive improvement points calmly and gracefully |

| Conflict Resolution | Sort out differences peacefully without harming teamwork |

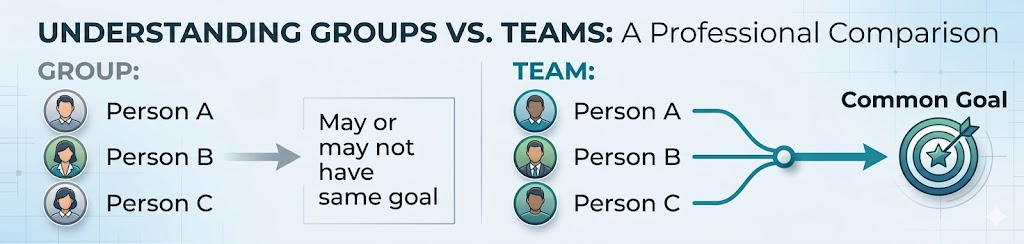

1.2 Difference between Teams and Groups

A group consists of individuals who share common characteristics but may or may not have common goals. A team, however, always works towards a shared common goal.

The football team is a good example — all players work towards the single goal of winning against the other team.

1.3 Benefits of Teamwork

- Higher Productivity: Humans work faster and more effectively when working together.

- Better Cooperation: Team members can learn from each other’s mistakes and support one another.

- Creativity and Problem Solving: Team members can bring unique skill sets together to tackle challenges.

- Sharing of Work: The work burden is divided, reducing stress on any single person.

- Learning and Motivation: Everyone learns from one another, staying motivated and focused.

Unit 1: Self-Test Questions – Solutions

Choose the correct option:

- Which of the following is an example of a team?

- Answer: c. Army regiment — An army regiment has soldiers working toward a common defence goal.

- Which of the following distinguishes a team from a group?

- Answer: c. A team works towards a common purpose, but a group does not.

Fill in the blanks:

- Excellent and ________ teams make challenging tasks achievable and straightforward.

- Answer: a. Effective

- For a team to work efficiently, team members should ________ with each other properly.

- Answer: b. Communicate

- Members need to show conflict resolution skills to sort out the ________ peacefully.

- Answer: b. Differences

True or False:

- Teams work well when there are differences among the members. — False (Teams work well when there is harmony.)

- Feedback should be taken or given while working in a team to avoid conflicts. — True

- Humans tend to work slower in a team. — False (Humans work faster and more effectively in a team.)

Unit 2: Introduction to Financial Literacy

2. Introduction to Financial Literacy

How often do we see our parents planning monthly budgets for groceries, house rent, and school fees? The possession of financial knowledge and skills that help us make intelligent financial decisions is called financial literacy.

2.1 Understanding Basic Financial Concepts

| Term | Meaning |

|---|---|

| Money | A recognised medium of exchange in the economy; an asset stored as currency or in accounts |

| Currency | Physical form of money in coins and notes; in India, issued by GoI and RBI |

| Bank | A government-authorised financial institution that accepts deposits and gives loans |

| Account | A repository of funds held by a bank on behalf of the account holder; identified by a unique account number |

In India, our currency is the Rupee (₹). We use it to buy things ranging from food at the school canteen to high-value products like cars.

2.2 Barter System

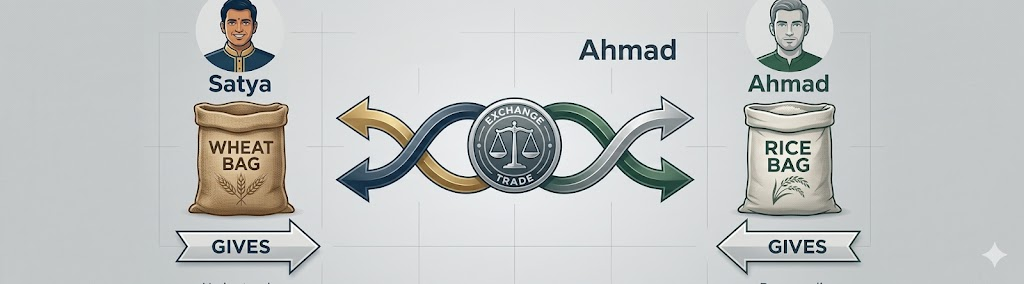

Before money was invented, people traded goods for goods. This is called the Barter System.

A simple example:

- Satya has two bags of wheat but needs only one.

- Ahmad has two bags of rice but can spare one.

- They exchange one bag each — Satya gets rice and Ahmad gets wheat.

Even today, simple barter happens in daily life. For example, you give your video game to your sister and she lends you her toys.

2.3 Needs and Wants

| Term | Meaning | Examples |

|---|---|---|

| Needs | Essential requirements for life | Food, clothes, house |

| Wants | Things that enhance the quality of life | Games, music, TV, juice, popcorn |

When you feel hungry, food is a need. When you want fruit juice at a school picnic, that is a want — enjoyable, but not essential.

2.4 Evolution of Trade and Commerce

Trade is the basic economic activity of buying and selling goods and services. For example, buying a loaf of bread from a shop.

Commerce includes all activities that support buying and selling — from manufacturing to delivery:

- Transportation of bread from bakery to store

- Payment from shopkeeper to bread maker

- Advertisement display in the shop

- Payment from customer to shopkeeper

Did You Know? The Han Dynasty (206 BC–220 AD) opened the famous Silk Road trade route between China and Central Asia — one of the world’s oldest international trade routes.

2.5 Concept of Cash Memo

When you purchase groceries from a local store, the shopkeeper gives you a receipt. This is a cash memo.

- A cash memo is used in cash transactions.

- It acts as proof of cash sales.

- Both the seller and buyer document their transaction to avoid future confusion.

Unit 2: Self-Test Questions – Solutions

Choose the correct option:

- What is the benefit of being financially literate?

- Answer: a. Financial literacy helps us make intelligent financial decisions.

- Which of the following is NOT a need?

- Answer: d. Car (A car is a want, not an essential need.)

Fill in the blanks:

- Cash memo acts as __________ in any business or transaction.

- Answer: a. Proof of cash sales

- The _________________ opened up the ‘Silk Road’ trading route.

- Answer: c. Han Dynasty

Unit 3: Banking

3. Banking

Imagine a person lending money to another without any documentation. If the borrower refuses to pay back, the lender has no proof to act upon. A bank solves this problem — it is a financial system licensed by the governing authority to lend money and receive deposits, maintaining all proper documentation and charging interest on loans.

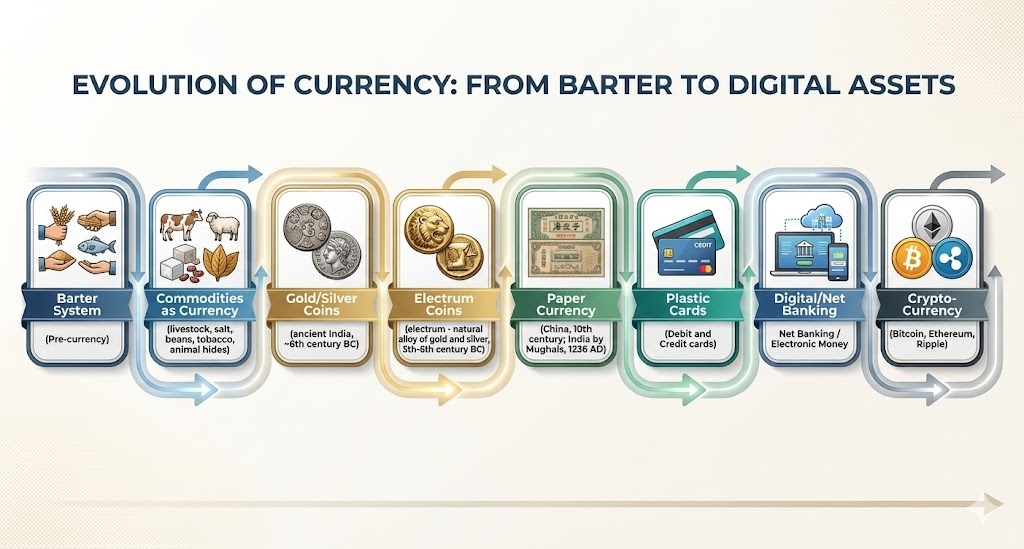

3.1 Evolution of Money

The limitations of the barter system led to the development of money. Here is how money evolved over time:

3.2 Banks and Their Importance

A bank acts as a vault for the safe-keeping of funds. It also provides loans to deposit holders who need extra funds.

Banks play an essential role in national development:

- Provide loans to farmers, service members, business people, and organisations.

- Convert savings into investments.

- Raise the standard of living through loans for homes, automobiles, and consumer goods.

- Support backward regions through adequate funds at reasonable interest rates.

3.3 Origins of Banking

Banking started in ancient temples and palaces before 2000 BC, where people stored jewels and precious items. Ancient Greeks also developed a system of transferring money through book entries.

Modern banking in India — Timeline:

| Year | Event |

|---|---|

| 1770 | Bank of Hindostan — first modern bank in India |

| 1806 | Bank of Calcutta (later Bank of Bengal) |

| 1840 | Bank of Bombay |

| 1843 | Bank of Madras |

| 1921 | All three merged to form Imperial Bank of India |

| 1955 | GoI and RBI nationalised it; renamed State Bank of India (SBI) |

SBI is the oldest surviving bank of India.

3.4 Types of Banks

| Type | Description | Example |

|---|---|---|

| Central Bank | Most important institution; manages monetary policy | Reserve Bank of India (RBI) |

| Public Sector Banks | Nationalised/government-owned banks | SBI, Punjab National Bank |

| Private Sector Banks | Privately owned commercial banks | HDFC, ICICI, Axis Bank |

| Foreign Banks | Banks from other countries operating in India | National Australia Bank, American Express |

| Regional Rural Banks (RRBs) | Banks serving rural areas | Various state RRBs |

12 Nationalised Banks in India:

- State Bank of India

- Bank of India

- Bank of Maharashtra

- Canara Bank

- Indian Overseas Bank

- Punjab & Sind Bank

- Punjab National Bank

- UCO Bank

- Bank of Baroda

- Union Bank of India

- Indian Bank

- Central Bank of India

3.5 Opening a Bank Account

To open a bank account, applicants submit:

- Passport-size photographs

- Identity proof

- Address proof

- Opening amount

Once opened, the bank provides an account number and a cheque book.

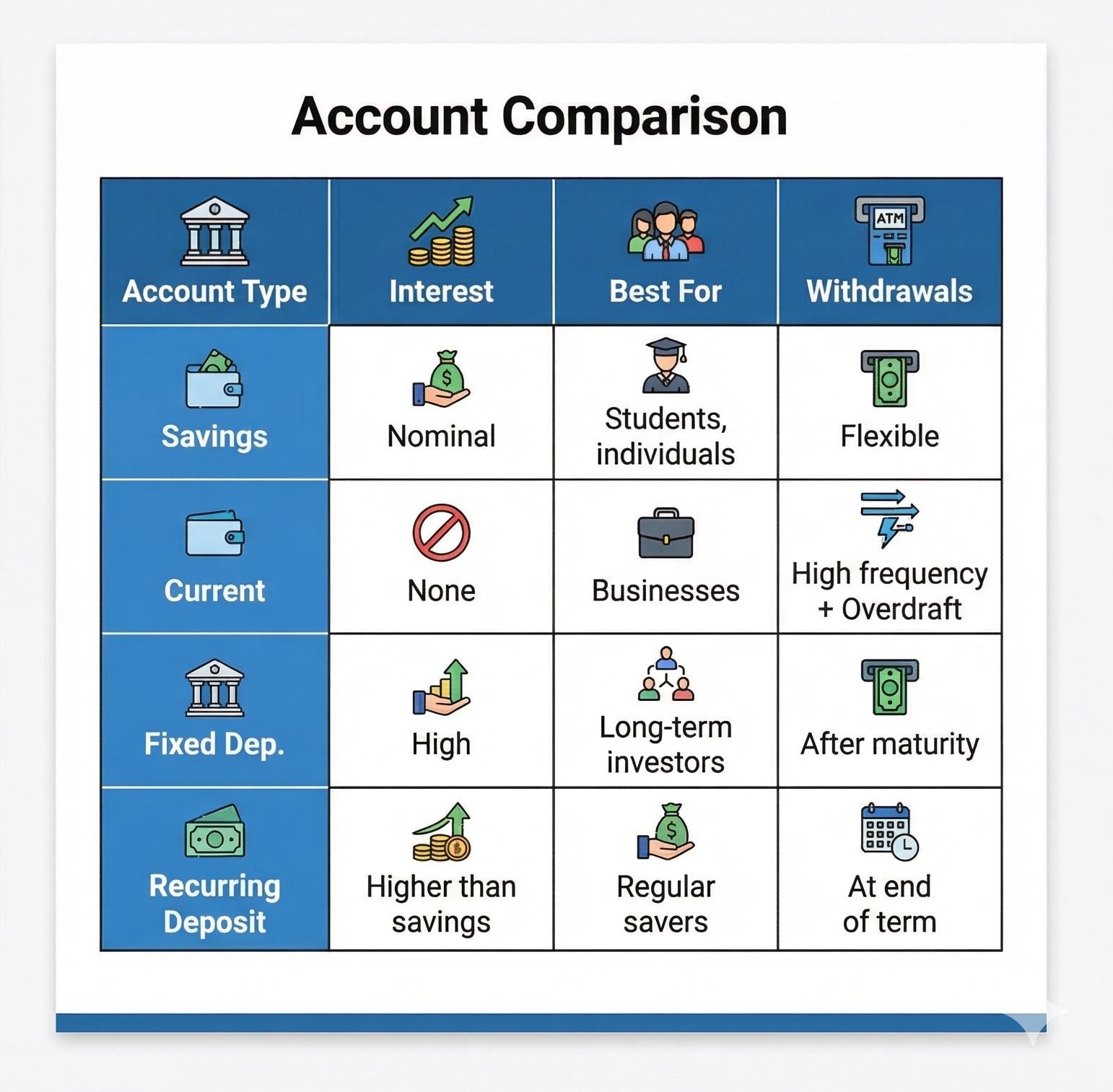

3.6 Types of Bank Accounts

3.6.1 Savings Account

- For developing saving habits.

- Maximum flexibility to deposit any amount.

- Popular with students, salaried individuals, and senior citizens.

- Earns a nominal interest based on the period of deposit.

3.6.2 Current Account

- For business owners with high transaction needs.

- Does not earn interest.

- Provides overdraft facility — withdrawing more than the account balance; interest is charged on the overdraft amount.

3.6.3 Fixed Deposit

- For depositors who want to park funds for an extended period.

- Offers a substantially higher interest rate than savings accounts.

3.6.4 Recurring Deposit

- Popular with students.

- A fixed amount is deposited every month for a set period.

- Example: Depositing ₹1,000 per month for 24 months = Base amount ₹24,000 + Interest received at maturity.

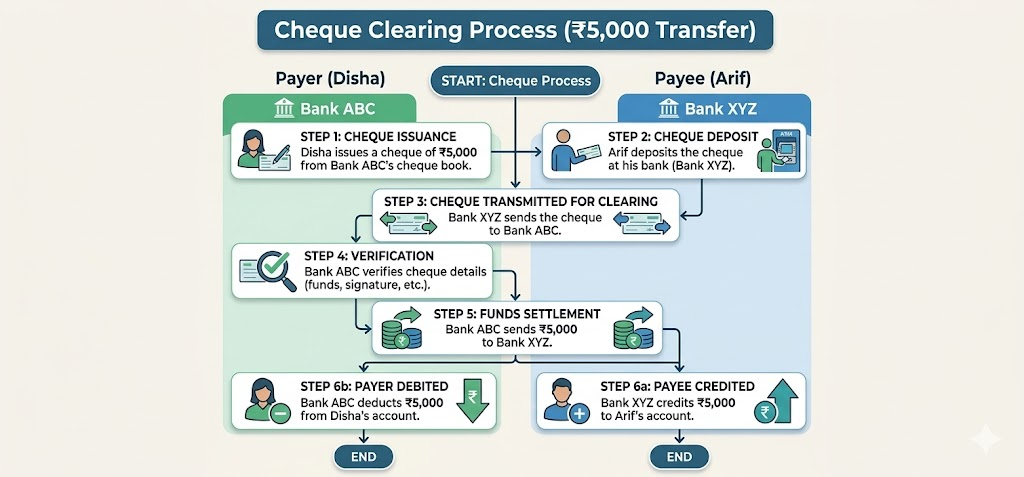

3.7 Cheque – An Instrument of Exchange

A cheque is a written instruction from the account holder to the bank to pay a certain amount to a named person.

How cheques work — Example (Disha pays Arif ₹5,000):

Imp elements on every cheque:

- Amount in words and numbers

- Name and signature of the account holder

- Name of the person receiving payment

- The date on or after which the cheque is valid

Unit 3: Self-Test Questions – Solutions

Choose the correct option:

- Which is ideal for depositors who wish to park funds long-term?

- Answer: b. Fixed deposit

- Which amongst the following is NOT a commercial bank?

- Answer: a. EXIM Bank (EXIM Bank is an export-import bank, not a commercial bank.)

- This account allows maximum flexibility to deposit any amount.

- Answer: b. Savings account

Match the following:

| Number | Term | Correct Match |

|---|---|---|

| 1 | Public sector banks | C – Owned by the government |

| 2 | Cheque | A – An instrument for money transfer |

| 3 | Recurring deposit | D – Regular savings amongst people |

| 4 | Evolution | B – Coins to paper currency |

Guess the words:

- Allowance to withdraw more than account balance → OVERDRAFT

- For safekeeping of funds, a bank acts as a → VAULT

Unit 4: Security

4. Reserve Bank of India – Role and Importance

Established in 1935 and nationalised in 1949, the Reserve Bank of India (RBI) is India’s central bank. It issues currency and also destroys worn-out notes and coins.

Imp functions of RBI:

- Monetary management authority — regulates prices and keeps inflation in check.

- Banker and debt manager to the Government of India.

- Banker to all other banks in India.

- Body for financial regulation and supervision.

- Manages foreign exchange reserves.

- Supervises market operations, payment systems, and research.

4.1 About NPCI

National Payments Corporation of India (NPCI) is a not-for-profit organisation that builds India’s retail payments and settlement infrastructure. It is an initiative of the RBI and Indian Banks’ Association (IBA).

NPCI’s shareholders include public sector banks, private banks, foreign banks, RRBs, cooperative banks, payments banks, payment system operators, and small finance banks.

4.2 Digital India and Aatmanirbhar Bharat Abhiyan

Digital India is a flagship government programme for the digital transformation of India’s economy. Its components include:

| Category | Initiatives |

|---|---|

| Digital Identity | Aadhaar |

| Digital Governance | eTaal |

| Digital Platforms | GSTN, GeM, DigiLocker, UMANG |

| Digital Payments | UPI, USSD, Bharat QR, NACH, IMPS, NETC, RuPay, BBPS, BHIM, AePS, BHIM Aadhaar Pay |

| Digital Infrastructure | BharatNet, National Knowledge Network, Meghraj |

| Digital Inclusion | Common Service Centres (CSCs), Stree Swabhiman, Rural BPOs |

4.2.1 Aatmanirbhar Bharat Abhiyan

Aatmanirbhar Bharat Abhiyan (Self-reliant India Mission) aims to make India a global economic powerhouse.

Its features include:

- Credit boost to farmers

- IT for healthcare

- Public distribution system access

- Online education through technology

- Employment through MGNREGA

- Support for MSMEs

- Ease of doing business reforms

- Corporate law and financial sector measures

- Reforms in power, space, coal, mining, and civil aviation sectors

4.3 Introduction to Digital Banking

Digital banking allows bank customers to avail banking services using the bank’s website or a mobile app. The 4G network expansion and widespread use of smartphones have made digital banking widely accessible.

Services available through digital banking:

- Checking account balance

- Transferring funds to another account

- Ordering a cheque book

- Changing passcodes

4.4 Understanding Digital Payments

Digital Payments means transferring money to another person, business, or organisation through the internet — without handling physical cash.

Sender → [Internet / Mobile App] → Receiver

No physical cash handled

Unique Transaction ID generated

4.5 Benefits of Digital Payments

| Benefit | Description |

|---|---|

| Fast, easy and convenient | Make payments anytime using just a smartphone; no travel required |

| One-stop solution | Pay bills, buy goods, send money — all in one platform |

| Digital record | Each transaction has a unique ID; fully secure with minimal risk |

| Transparent transactions | No cash handling; discourages black money; all transactions tracked |

Unit 4: Self-Test Questions – Solutions

Choose the correct option:

- This bank issues currency in India and also destroys unfit notes and coins.

- Answer: a. RBI

- What has made digital banking possible?

- Answer: c. The vast expansion of 4G Network

- Digital payment helps to discourage the use of:

- Answer: b. Black money

True or False:

- A unique transaction ID backs each digital transaction. — True

- Digital Payments involves transferring money with the help of cash. — False (It is cashless.)

- Digital India is a programme to transform India into a digitally empowered economy. — True

Answer the following:

- List the benefits of Digital Payments.

- Fast, easy and convenient

- One-stop solution

- Digital record (unique transaction ID)

- Transparent transactions (discourages black money)

- List the services available through digital banking.

- Checking account balance

- Transferring funds to another account

- Ordering a cheque book

- Changing passcodes

Unit 5: Modes of Digital Payments – Card Based

5. Modes of Digital Payments – Card Based

Digital payments made using plastic cards are called card-based digital payments.

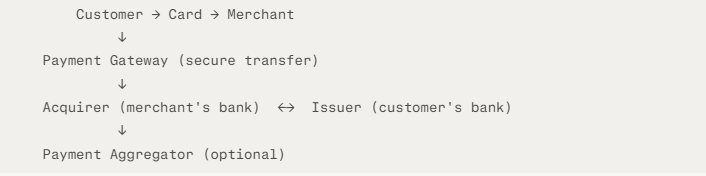

5.1 Payments Acceptance Ecosystem

The payment acceptance ecosystem has four components:

| Component | Role | Example |

|---|---|---|

| Acquirer | Bank that contracts with merchants to accept card payments; installs PoS machines | SBI Merchant Services |

| Issuer | Bank that issues debit/credit cards to customers | HDFC Bank |

| Payment Gateway | Securely transfers payment information between customer and merchant | Secure server link |

| Payment Aggregator | Enables e-commerce merchants to accept multiple payment modes without a separate bank account | Razorpay, PayPal, PayTM |

5.2 Use of Banking Cards

5.2.1 Debit Cards

- Dual purpose: ATM transactions (deposit, withdrawal, account info) and cashless payments at shops.

- The purchase amount is directly deducted from the linked bank account.

5.2.2 Credit Cards

- Provide instant credit to the cardholder.

- Amount is not deducted from the bank account immediately — it is given as credit.

- Cardholder has generally one month to repay.

- Banks charge interest on amounts not repaid within the stipulated time.

5.2.3 Prepaid Cards

- Stored value cards charged with a specific amount.

- Example: A card loaded with ₹5,000 — once that value is used, more value must be added.

- Examples: Gift card, Meal card, Salary card.

5.2.4 Virtual Cards

- One-time, non-physical cards issued for a single online transaction.

- Exist only in digital form; expire automatically after use.

- Ideal for minimising risk in online transactions.

5.2.5 Co-branded Cards

- Issued through collaboration between a bank and a retailer/service provider.

- Carry logos of both parties.

- Provide reward points or cashback on purchases.

- Example: A petrol credit card that gives cashback on fuel purchases.

5.3 Guidelines for the Use of Banking Cards

- Be observant at ATMs — ensure no one is watching you enter your PIN.

- Pay credit card dues on time to avoid heavy interest.

- Keep banking cards safe and out of the wrong hands.

- Never share card PIN numbers with anyone.

5.4 Channels for Acceptance of Card-Based Digital Payments

5.4.1 Point of Sales (PoS)

PoS is a system that automatically tracks each sale transaction, the customer’s amount, and inventory — replacing paper-based record keeping.

Imp benefits of PoS:

| Benefit | Description |

|---|---|

| Faster Process | Removes rush at the cash counter; makes process efficient |

| Inventory Management | Track product and stock status at a button’s press |

| Sales Report | Generate accurate sales reports at any time |

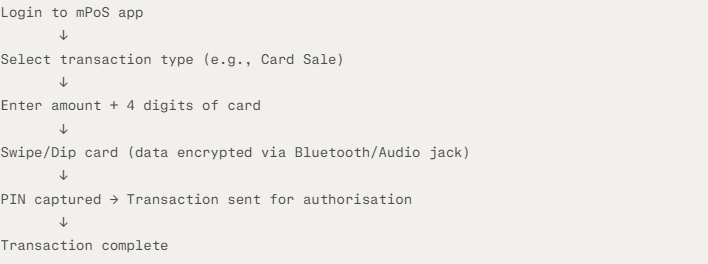

5.4.2 mPoS – Mobile Point of Sales

mPoS uses a mobile phone-based Java/iOS application for card payments. Once the card is swiped:

5.4.3 Soft PoS

Soft PoS uses Tap-on-Phone (NFC) technology. Merchants accept contactless card payments directly on their NFC-enabled Android mobile — no extra hardware needed. Affordable and enables wider market reach.

5.4.4 E-commerce Payment

Online PoS used for internet-based transactions through net banking or banking cards. India’s e-commerce industry is a multi-billion dollar industry with a vast customer base.

5.4.5 Automated Teller Machines (ATMs)

ATMs allow customers to withdraw cash and perform banking transactions at any time, without visiting a bank branch.

Benefits to Banks:

- Increases customer satisfaction (24×7 access)

- Reduces crowding at bank branches

- Enhances customer loyalty

- Interoperability allows customers to use any bank’s ATM

Benefits to Customers:

- Fewer visits to a bank branch

- Convenient access to cash 24×7

- Balance inquiry, mini statement, PIN change

- Use any bank’s ATM with an interoperable card

5.4.6 Types of ATM Deployments

| Feature | White Label ATMs (WLAs) | Brown Label ATMs (BLAs) |

|---|---|---|

| Ownership | Non-banking financial institutions (authorised by RBI) | Hardware owned by service provider |

| Branding | No specific bank branding (some show WLA + partner logo) | Carries sponsor bank’s logo |

| Cash | Provided by sponsor bank | Provided by sponsor bank |

| Common in | Smaller and remote towns | Regular locations |

| Customer experience | Same as a regular ATM | Same as a regular ATM |

5.5 About RuPay Network and RuPay Card

RuPay is India’s domestic card payment network, developed and launched by NPCI in 2012. It provides a financial benefit to both people and banks — banks pay lower service charges compared to international payment networks.

Unit 5: Self-Test Questions – Solutions

Choose the correct option:

- What is a PoS?

- Answer: b. A system that automatically keeps track of each sale transaction and the customer’s amount.

- These cards are stored value cards.

- Answer: c. Prepaid Cards

True or False:

- Soft PoS is an innovative payment acceptance segment that uses ‘Tap-on-Phone’ technology. — True

- ATMs offer benefits to customers but not to banks. — False (ATMs benefit both customers and banks.)

Identify the hidden terms (Word Search answers):

- Debit Cards

- Banks

- PIN

- Credit Cards

- ATM

- Digital

Unit 6: Modes of Digital Payments – Biometric Based

6. Modes of Digital Payments – Biometric Based

Biometric-based digital payment systems in India include:

- Aadhaar Enabled Payment System (AePS)

- Micro ATMs

- Bharat Interface for Money (BHIM) Aadhaar Pay

6.1 Role of UIDAI

The Unique Identification Authority of India (UIDAI) was formed by the Government of India in January 2009. UIDAI issues Unique Identification numbers (UID) — called Aadhaar — to all residents of India.

Imp objectives of UIDAI:

- Eliminate duplicate and fake identities.

- Provide a verifiable and authenticable identity in a comfortable, cost-effective manner.

6.2 Aadhaar Enabled Payment System (AePS)

AePS is a payment service operated by NPCI that uses Aadhaar biometric authentication. It helps achieve the financial inclusion goal of the Government of India and RBI.

AePS empowers bank customers to perform basic banking transactions using just their Aadhaar:

- Balance enquiry

- Cash deposit

- Cash withdrawal

- Aadhaar to Aadhaar funds transfer

- Mini Statement

- Digital payment through BHIM Aadhaar

6.2.1 AePS Features

Financial Transactions:

- Balance Enquiry

- Cash Withdrawal

- Cash Deposit

- Fund Transfer

- Mini Statement

- BHIM Aadhaar

Non-Financial Transactions:

- Best Finger Detection

- eKYC (Know Your Customer digitally)

- Demographic Authentication

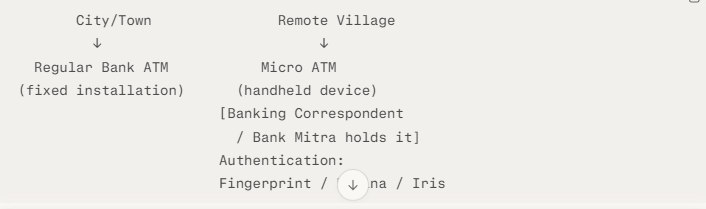

6.3 Micro ATMs – Perfect Solution for Rural Areas

Regular ATMs are not available in remote and rural areas of India. Micro ATMs fill this gap.

Imp features of Micro ATMs:

- Portable and handheld — ideal for remote locations.

- Available with authorised banking correspondents (Bank Mitras).

- Can be purchased and activated at a fraction of a conventional ATM’s cost.

- Can be made compatible with regional languages.

- AePS drives financial inclusion in rural areas — people no longer need to travel long distances for banking.

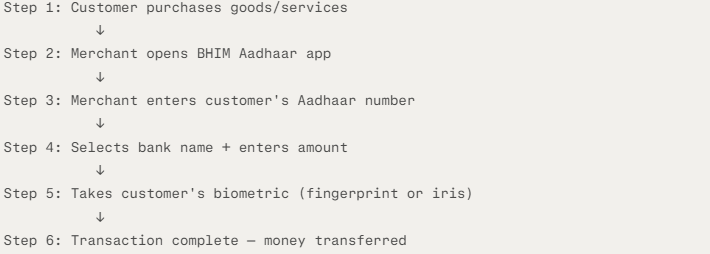

6.4 BHIM Aadhaar Pay – The Merchant Solution

BHIM Aadhaar Pay lets merchants receive digital payments from customers using Aadhaar biometrics — no debit or credit card needed.

What the merchant needs:

- An Android mobile with the BHIM Aadhaar app

- A certified biometric scanner connected to PoS, mPoS, or Micro ATM

How BHIM Aadhaar Pay works:

Customer requirement: Aadhaar number linked to their bank account.

Unit 6: Self-Test Questions – Solutions

Choose the correct option:

- What are the critical objectives of UIDAI?

- Answer: a and b — Eliminate fake and duplicate identities; Authenticate individuals in a comfortable and cost-effective way.

- Which of the following is needed to enable BHIM Aadhaar Pay?

- Answer: a, b, and c — Android mobile, BHIM Aadhaar app, and Certified Biometric Scanner.

True or False:

- Digital technology has made financial transactions more straightforward and convenient. — True

- Compared to a conventional ATM, a Micro ATM cannot be purchased at a fraction of the cost. — False (Micro ATMs cost far less than conventional ATMs.)

- AePS empowers bank customers to access their Aadhaar-enabled bank account for basic transactions. — True

Answer the following:

- What are the biometric-based digital payment systems in India?

- Aadhaar Enabled Payment System (AePS)

- Micro ATMs

- Bharat Interface for Money (BHIM) Aadhaar Pay

- Write about BHIM Aadhaar Pay in your own words:

- BHIM Aadhaar Pay is a payment solution for merchants that allows them to receive digital payments from customers using the customer’s Aadhaar number and biometric (fingerprint or iris) authentication. The merchant uses a BHIM Aadhaar app on an Android phone and a certified biometric scanner. No card is needed by the customer — just their Aadhaar linked to their bank account.

Unit 7: Modes of Digital Payments – Mobile Based Banking and Others

7.1 Internet Banking

Internet banking allows banking activities over the internet using a laptop, tablet, or smartphone. Account holders can transfer funds to a beneficiary at any time without cheques.

Internet banking transfer methods:

| Method | Full Form | Operated by | Transfer Limit | Key Feature |

|---|---|---|---|---|

| NEFT | National Electronic Fund Transfer | RBI | No fixed limit | Operates in half-hourly batches; pan-India coverage |

| RTGS | Real-Time Gross Settlement | RBI | Min ₹2,00,000; no upper limit | Real-time, irrevocable; for large-value transactions |

| IMPS | Immediate Payment Service | RBI + NPCI | Max ₹2 lakh per transaction; min ₹1 | 24×7 instant transfer; works on mobile, internet, ATM, SMS |

7.1.1 National Electronic Fund Transfer (NEFT)

NEFT is a centralised payment system owned and operated by RBI. Before transferring, the sender must register the beneficiary’s: account holder name, account type, account number, and IFSC code.

Imp advantages:

- Available round the clock, all days of the year.

- Near-real-time transfer; confirmation via SMS/e-mail.

- Pan-India coverage across all bank branches.

IFSC = Indian Financial System Code — an 11-digit alphanumeric code unique to each bank branch.

7.1.2 Real-Time Gross Settlement (RTGS)

RTGS is primarily for large value transactions. “Real Time” means instructions are processed the moment they are received. “Gross Settlement” means each transfer is settled individually.

Payments via RTGS are final and irrevocable (cannot be reversed).

Imp advantages:

- Safe and secure.

- No cap on maximum amount.

- Available 24x7x365.

- Real-time transfer.

7.1.3 Immediate Payment Service (IMPS)

IMPS is available 24×7 including holidays. Funds can be sent using just the beneficiary’s mobile number and MMID (Mobile Money Identifier) — no bank account number required.

Imp advantages:

- Works on net banking and mobile platforms.

- Transfer confirmation sent to both payer and payee.

- Maximum ₹2 lakh per transaction; minimum ₹1.

7.2 Mobile Banking – Bank in Pocket

Most popular banks offer a secure dedicated mobile app providing:

- Account balance checking

- Funds transfer

- Bill payments and card payments

- Service requests like ordering cheque books

7.2.1 Advantages of Mobile Banking

- 24x7x365 access to banking services.

- Saves time and money by avoiding branch visits.

- Better control over account and finances.

- Reduces paperwork through digital technology.

7.2.2 Do’s and Don’ts while Using Mobile Banking

| Do’s | Don’ts |

|---|---|

| Use only the bank-authorised mobile banking app | Do not use fake apps that steal identity |

| Keep a strong password/PIN | Do not share PIN or OTP with anyone |

| Keep your mobile free from malware | Do not install apps from non-secure sources |

7.3 Unified Payments Interface (UPI)

UPI is a system developed by NPCI that combines the power of multiple bank accounts into a single mobile app.

A UPI ID is a unique payment address — just like an email address — used to send or receive money. Example: abcd@upi.

Imp features of UPI:

- Easy, safe, and instant transactions.

- Access multiple bank accounts from one app.

- Send/receive money across 200 banks and 21 third-party apps.

- Direct bank payments using UPI ID or UPI QR.

- Single-click authentication using UPI PIN.

- Covers daily expenses, e-commerce, bill payments, and more.

7.4 Bharat Interface for Money (BHIM)

BHIM is a digital app for making simple, easy, and quick payments using UPI.

Imp features of BHIM:

- Send money

- Request money

- Scan QR code and pay

- Bill payments

- UPI AutoPay

- Biometric Authentication

- Supports 20 languages

- Balance Enquiry

7.4.1 Steps for First Time BHIM User

- Download BHIM app from Google Play Store or Apple App Store.

- Select preferred language.

- Read and allow necessary app permissions.

- Select the SIM card linked to your bank’s registered mobile number.

- Set an application passcode.

- Link your bank account via the bank account option.

- Set UPI PIN using the last six digits of your debit card and its expiry date.

- To send money, tap Send → enter UPI ID or scan QR code or enter Account/IFSC.

- Enter amount and the account to debit → tap Send.

- Enter UPI PIN to authenticate → transaction complete.

Important: Never share OTP, debit card details, or UPI PIN with anyone.

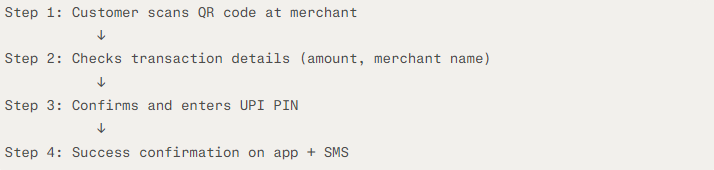

7.5 QR Codes – An Easy Way to Pay

A QR (Quick Response) code is a type of barcode. UPI makes paying via QR codes very convenient:

A barcode is an optical label on physical goods that a barcode reader can scan.

7.6 Mobile Wallets – The Smart Way to Make Payments

A mobile wallet is a virtual wallet in the form of a mobile app that allows purchases by scanning the QR code at a merchant. A popular example is PayTM.

Imp benefits of mobile wallets:

- Make payments using a mobile without carrying cash or cards.

- Pay utility bills conveniently.

- Transactions are fast with instant confirmation for both sender and receiver.

- Secure, authenticated user platforms.

7.7 Unstructured Supplementary Service Data (USSD)

USSD is a technology for people without smartphones or internet access. Using the code *99#, anyone with a basic mobile phone can access mobile banking services.

USSD is available in 12 languages — English, Hindi, Tamil, Bengali, Kannada, and others.

Services available through USSD-based banking:

- Checking account balance

- Generating account statements

- Making funds transfers

7.8 Other Modes of Payments

7.8.1 National Automated Clearing House (NACH)

NACH is an electronic funds transfer system operated by NPCI for regular, recurring transactions.

Types of NACH:

| Type | Description | Example |

|---|---|---|

| NACH Debit | A specific amount deducted from account regularly | Loan EMI, mutual fund investment |

| NACH Credit | A specific amount credited regularly | Monthly salary to employees |

| Aadhaar Payments Bridge System (APBS) | Payments based on Aadhaar number; government subsidies transferred directly to beneficiaries | DBT subsidies |

Imp advantages of NACH:

- Regular payment framework improves customer relationships.

- Reduces paper use.

- Reduces risk of delayed payments.

- Useful for insurance premiums, loan instalments, and mutual funds.

- Facilitates government subsidy distribution.

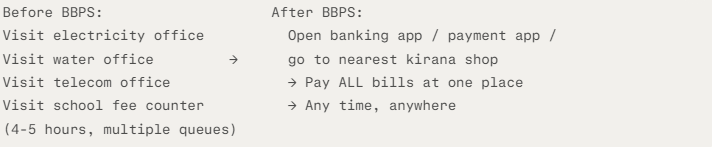

7.8.2 Bharat Bill Payment System (BBPS)

Before BBPS, consumers had to visit multiple payment centres, stand in long queues, and spend 4–5 hours paying various bills. NPCI, under RBI’s guidance, launched BBPS in 2017 as a one-stop solution for all recurring bills.

Bills payable via BBPS: electricity, telecom, DTH, gas, water, taxes, loan repayments, school/college fees, and more.

Unit 7: Self-Test Questions – Solutions

Choose the correct option:

- It allows 24×7 instant funds transfer across multiple channels like Mobile, Internet, ATM, and SMS.

- Answer: b. IMPS

- It combines multiple bank accounts’ power into a single mobile app.

- Answer: b. UPI

- Which of the following bills can be quickly paid using BBPS?

- Answer: d. All of the above (school fees, electricity bill, water bill)

True or False:

- UPI is a one-stop solution allowing a host of digital banking options and merchant payments. — True

- Transfers made via RTGS have an amount cap. — False (RTGS has no upper limit; only a minimum of ₹2 lakh.)

- BBPS cannot help in paying the gas bill. — False (BBPS covers gas bills.)

Answer the following:

- Essential services offered through USSD-based banking:

- Checking account balance

- Generating account statements

- Making funds transfers

- Features of BHIM:

- Send money, Request money, Scan QR code and pay, Bill payments, UPI AutoPay, Biometric Authentication, supports 20 languages, Balance Enquiry.

- Describe UPI in your own words:

- UPI stands for Unified Payments Interface. It is a system by NPCI that links multiple bank accounts into a single mobile app. Using a UPI ID — which is a unique payment address like an email — users can instantly send or receive money to or from any UPI-enabled app or bank. UPI supports payments at shops, for bills, and for online shopping through a single click authentication using a UPI PIN.

Imp Abbreviations – Full Reference Table

| Short Form | Full Form |

|---|---|

| GoI | Government of India |

| RBI | Reserve Bank of India |

| NPCI | National Payments Corporation of India |

| SBI | State Bank of India |

| RRBs | Regional Rural Banks |

| UPI | Unified Payments Interface |

| GSTN | Goods and Services Tax Network |

| GeM | Government e-Marketplace |

| UMANG | Unified Mobile App for New-Age Governance |

| NETC | National Electronic Toll Collection |

| BBPS | Bharat Bill Payment System |

| BHIM | Bharat Interface for Money |

| AePS | Aadhaar Enabled Payment System |

| CSC | Common Service Centre |

| MSME | Micro, Small, and Medium Enterprise |

| NBFC | Non-Banking Finance Companies |

| USSD | Unstructured Supplementary Service Data |

| QR | Quick Response |

| NACH | National Automated Clearing House |

| IMPS | Immediate Payment Service |

| NEFT | National Electronic Fund Transfer |

| RTGS | Real-Time Gross Settlement |

| IFSC | Indian Financial System Code |

| PIN | Personal Identification Number |

| OTP | One Time Password |

| UIDAI | Unique Identification Authority of India |

| UID | Unique Identity |

| PoS | Point of Sales |

| mPoS | Mobile Point of Sales |

| NFC | Near Field Communication |

| ATM | Automated Teller Machine |

| MMID | Mobile Money Identifier |

| APBS | Aadhaar Payments Bridge System |

| PAN | Permanent Account Number |

| DTH | Direct-to-Home |

| MGNREGA | Mahatma Gandhi National Rural Employment Guarantee Act |

Download Mind Map

This mind map contains all important topics of this chapter

Visit our Class 7 Skill Development page for free mind maps of all Chapters