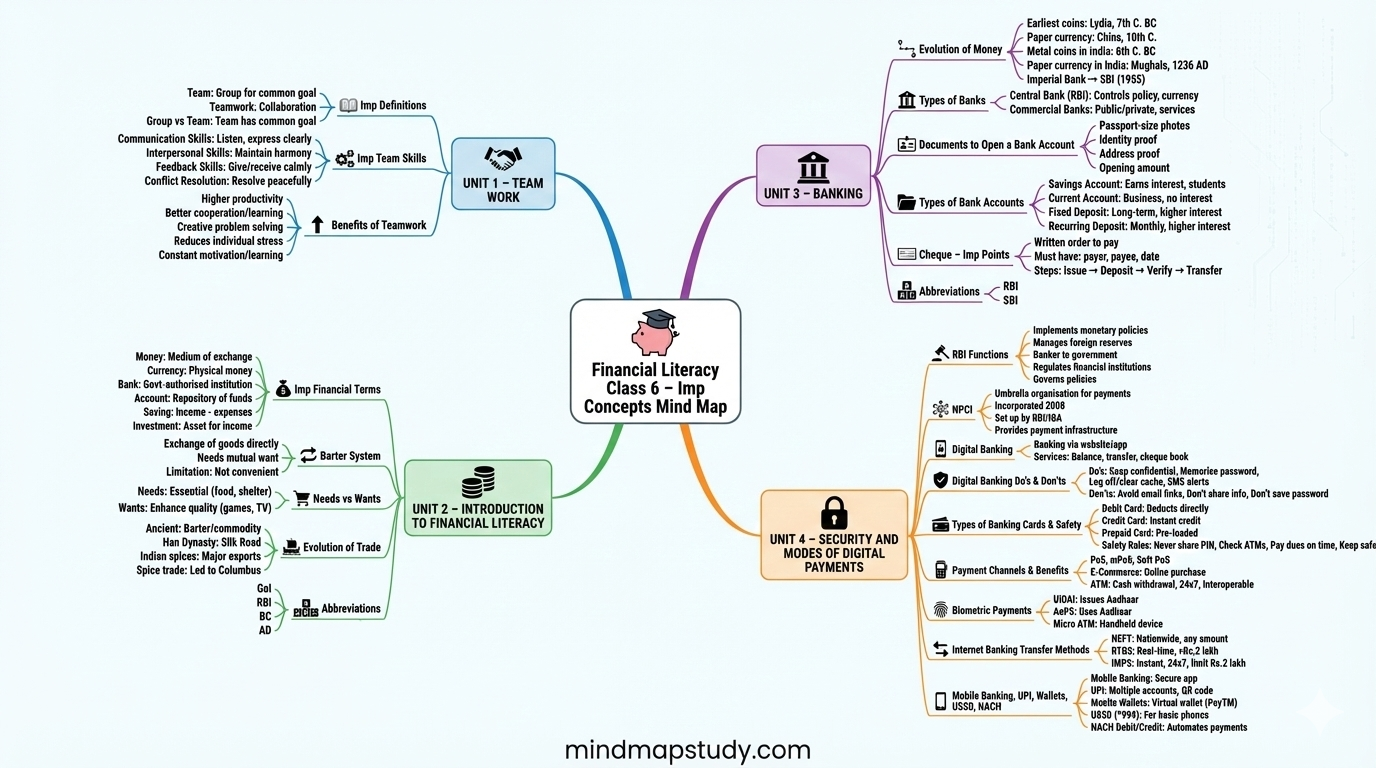

This Notes cover Teamwork, Introduction to Financial Literacy, Banking, and Security and Modes of Digital Payments.

Unit 1 – Team Work

1.1 Defining Team Work

A team is a group of people joined together to perform a common goal or objective. Teams can be formed in playgrounds, schools, and colleges. When members of a team perform some work together, it is called teamwork. Teamwork is a result of individuals working together in collaboration.

Tasks that may seem challenging alone become simpler when handled by a team. Each member contributes based on their own unique competencies. The output of a team is a combined result of all these distinct contributions, all working toward the same purpose.

1.2 Team Skills

For a team to work effectively, all members need to build and practise these skills:

- Communication Skills: Listen attentively and put across your thoughts and viewpoints clearly.

- Interpersonal Skills: Maintain harmony and positive relationships with fellow members.

- Feedback Skills: Share improvement points calmly and also receive feedback gracefully without getting upset.

- Conflict Resolution: Manage differences peacefully so that teamwork is not disrupted.

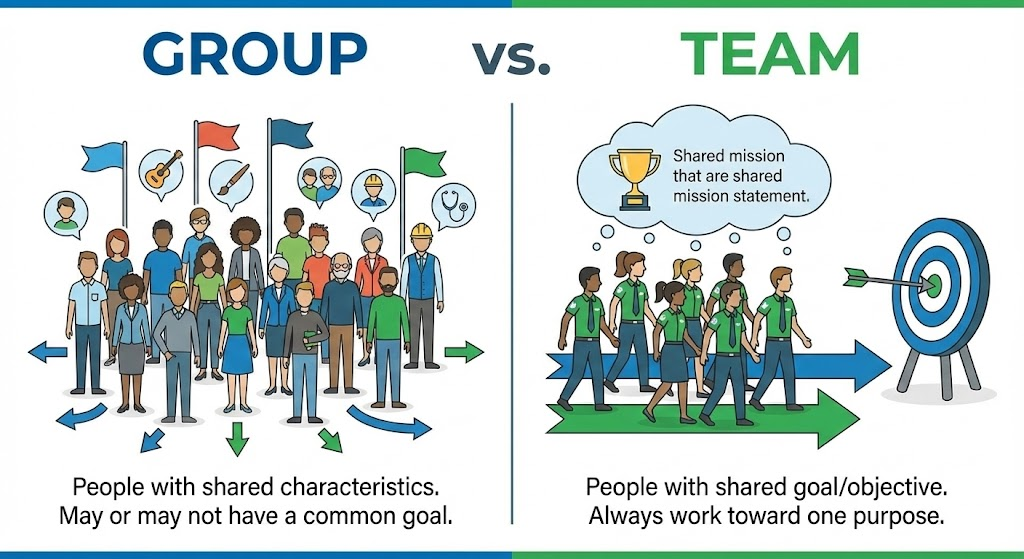

1.3 Teams and Groups

A group is a set of individuals with common characteristics, but they may or may not be tied to a common goal. A team is always tied to a common goal or objective. That is the one major difference.

Example: When you play football, all players on your side share the common goal of winning — that makes it a team, not just a group.

1.4 Benefits of Team Work

Working in a team brings multiple advantages:

- Higher Productivity: People work faster and more effectively together, as humans are naturally social beings.

- Better Cooperation: Team members learn from each other’s mistakes and offer support when needed.

- Creativity and Problem Solving: Different members bring unique skills that together produce more creative solutions.

- Sharing of Work: The work burden is divided among members, reducing individual stress.

- Learning and Motivation: Everyone learns new things from each other and stays motivated toward the shared goal.

Unit 1 – Self-Test Questions with Answers

Choose the Correct Option

1. Teams are sets of individuals bound with a common

a) Education b) Skill-set c) Objective

Answer: c) Objective

2. Which of the following is a valid example of a team?

a) Classroom b) Sports team c) Family

Answer: b) Sports team

Fill in the Blanks

1. A Team is a group of individuals who have a common ____________.

Answer: Goal or objective

2. While working in a team you must listen ____________.

Answer: Attentively

3. Working in a team allows for sharing of ____________.

Answer: Work

True or False

1. A team may or may not have a common objective.

Answer: False — A team always has a common goal or objective.

2. Communication skills are among the important skills required for effective teamwork.

Answer: True

3. Teamwork allows for better cooperation and sharing of work.

Answer: True

Unit 2 – Introduction to Financial Literacy

2.1 Understanding Basic Financial Concepts

Here are the core financial terms you need to know:

| Term | Meaning |

|---|---|

| Money | A recognised medium of exchange in the economy; can be stored as currency or value |

| Currency | Physical form of money in the form of coins and notes; issued by the central bank |

| Bank | A government-authorised financial institution that holds deposits and gives loans |

| Account | A repository of funds held by a bank on behalf of the account holder; has a unique number |

| Saving | The amount of money remaining from income after expenses are made |

| Investment | An asset acquired with the aim of generating income or appreciation |

In India, currency is issued by the Government of India (GoI) and the Reserve Bank of India (RBI) in the form of Indian Rupees.

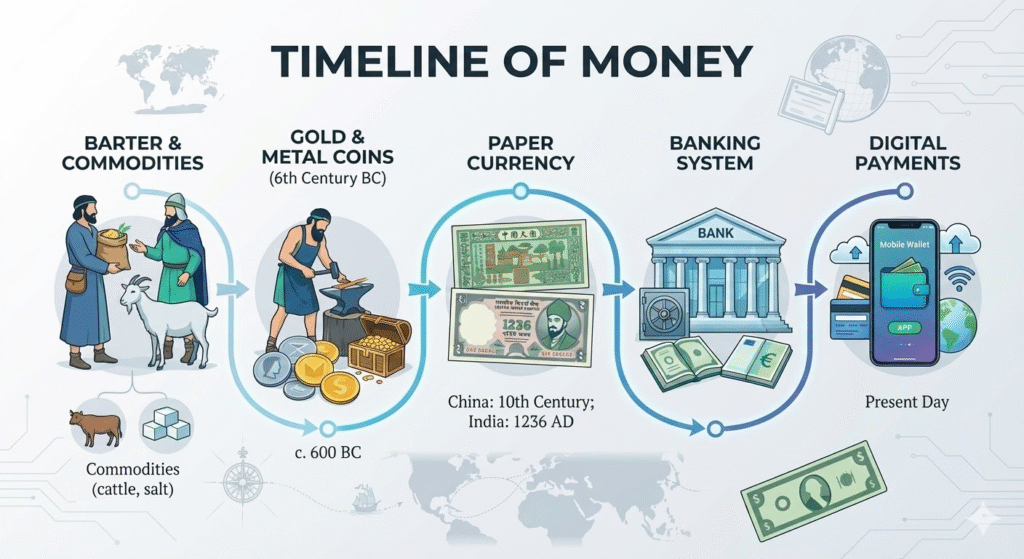

2.2 Barter System

Before money was invented, people exchanged goods directly. This was called the Barter System.

Example :

Both Satya and Ahmad now have what they need. That is how barter works. Even today, you may have informally done a barter — giving a friend your sketch pens in exchange for a geometry box.

Limitation of barter: It only works if both parties have what the other needs at the same time and place. This limitation led to the development of money.

2.3 Needs and Wants

Understanding needs and wants is important to manage money well.

| Needs | Wants | |

|---|---|---|

| Definition | Essential requirements for living | Things that enhance quality of life but are not essential |

| Examples | Food, clothing, shelter | Games, music, TV, ice cream |

| Nature | Cannot be done without | Can be managed without |

Example: When you are hungry, food is your need. But when you feel like having ice cream at a shop, that is your want.

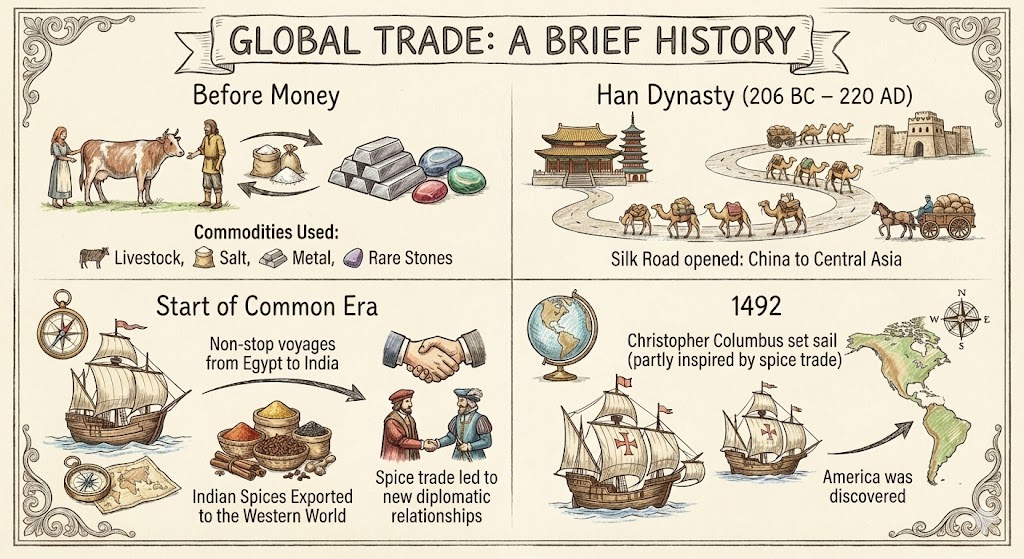

2.4 Evolution of Trade

Trade is a financial activity that involves buying and selling goods and services between two or more people, organisations, or countries.

India exports: rice, jewellery.

India imports: petroleum, electronic components.

Historical Timeline of Trade

The Silk Road was one of the oldest international trade routes in the world, carrying all types of merchandise between China and Central Asia.

Unit 2 Questions with Answers

Choose the Correct Option

1. In ancient trade, before the development of currency, the commodity of exchange used was

a) Coins b) Livestock c) Money

Answer: b) Livestock

2. In barter system, humans used to transact with the help of

a) Money b) Card c) Goods

Answer: c) Goods

Fill in the Blanks

1. _________ is a recognized medium of exchange in the economy.

Answer: Money

2. Currency is the _______ form of money.

Answer: Physical

3. In our country, money is used in the form of Indian currency known as _______.

Answer: Rupee

True or False

1. Our needs and wants are the same.

Answer: False — Needs are essential; wants are additional.

2. Money allows you to buy the things you require.

Answer: True

Answer the Following

1. What is trade?

Trade is a financial activity that includes buying and selling various goods and services between two or more people. Trade can happen between individuals, organisations, and countries.

2. Define Currency.

Currency is the physical form of money in the form of coins and rupee notes. It is issued by the central bank of a country. In India, currency is issued by the GoI and RBI in the form of Indian Rupees.

Abbreviations (Unit 2)

| Abbreviation | Full Form |

|---|---|

| GoI | Government of India |

| RBI | Reserve Bank of India |

| BC | Before Christ |

| AD | Anno Domini (in the year of the Lord) |

Unit 3 – Banking

3.1 Evolution of Money

The barter system had limitations — it required both parties to want what the other had. This led to the development of money.

Forms of Currency Used Across History

| Region / Era | Currency Used |

|---|---|

| Ancient India | Gold coins |

| Ancient Aztecs | Beans |

| Norwegians | Butter |

| US Colonists | Tobacco leaves and animal hides |

| Kingdom of Lydia (7th century BC) | First standardised coins |

| China (10th century) | First paper currency |

| Ancient India (6th century BC) | Metal coins |

| Mughal India (1236 AD) | Paper currency introduced |

3.2 Banks and their Importance

A bank is an institution where people deposit their funds as savings and can withdraw them when required. A bank acts as a vault for safekeeping of funds.

Banks also provide loans to deposit holders when they need more money than their savings — for purchasing a car, house, etc.

3.3 Origins of Banking

- Banking is said to have started in the temples and palaces of Babylonia before 2000 BC.

- Ancient Greeks developed a system of transferring money through book entries.

- Banking in India started in a major way with the Imperial Bank of India in 1921.

- It was later renamed the State Bank of India (SBI) in 1955.

3.4 Types of Banks

Central Bank

The Central Bank is the most important financial institution in any country.

- In India: Reserve Bank of India (RBI) is the central bank.

- Functions of RBI:

- Manages and issues currency.

- Acts as banker to the government.

- Implements monetary policies.

- Manages foreign exchange reserves.

- Provides financial regulation and supervision.

- Governs policies for all other banks.

Commercial Banks

- Include public sector banks (owned by government) and private banks.

- Provide direct services to people: open accounts, give loans, manage deposits.

3.5 Opening a Bank Account

To open a bank account, you need:

- Passport-size photographs

- Identity proof

- Address proof

- Opening amount (initial deposit)

After the account is opened, the bank provides:

- A unique account number

- A cheque book

- Access to mobile banking (with some banks)

3.6 Types of Bank Accounts

| Account Type | Purpose | Interest | Best For |

|---|---|---|---|

| Savings Account | Save money, build the habit of saving | Earns nominal interest | Students, salaried individuals, senior citizens |

| Current Account | Handle unlimited cash transactions daily | No interest earned; overdraft facility | Business owners |

| Fixed Deposit (FD) | Park funds for a long time | Higher rate than savings | Long-term depositors |

| Recurring Deposit (RD) | Deposit fixed amount every month | Higher than savings | Students, regular savers |

Example of Recurring Deposit:

Deposit: Rs.1000 per month

Duration: 24 months

Base amount at end: Rs.24,000

+ Interest earned on it

= Total received back

3.7 Cheque – An Instrument of Exchange

A cheque is a written order from the account holder asking their bank to pay a specific amount to another person.

How a Cheque Works (Step-by-step)

You have Rs.25,000 in Bank A.

You want to pay Rs.5,000 to Ajay.

Step 1: You issue a cheque of Rs.5,000 from Bank A's cheque book

Step 2: Ajay deposits it in his bank (Bank B)

Step 3: Bank B sends the cheque to Bank A

Step 4: Bank A confirms and sends Rs.5,000 to Bank B

Step 5: Rs.5,000 is credited to Ajay's account in Bank B

Step 6: Rs.5,000 is deducted from your account in Bank A

Imp Elements of a Cheque

- Name and signature of the account holder (payer)

- Name of the person receiving the payment

- Date on or after which the cheque is valid

Unit 3 – Self-Test Questions with Answers

Choose the Correct Option

1. Which account type is opened by business owners for unlimited deposits and withdrawals?

a) Savings Account b) Current Account c) Fixed Deposit

Answer: b) Current Account

2. For money withdrawal, a cheque must have:

a) Signature of recipient b) PAN card no. c) Signature of account holder

Answer: c) Signature of account holder

True or False

1. Commercial banks include public sector banks owned by the government.

Answer: True

2. Current account has a key purpose of inculcating the habit of saving among people.

Answer: False — That is the purpose of a Savings Account. Current Accounts are for businesses.

3. Fixed deposit provides a substantially higher rate of interest.

Answer: True

Answer the Following

1. List down the names of bank accounts:

- Savings Account

- Current Account

- Fixed Deposit (FD)

- Recurring Deposit (RD)

2. Describe about cheque in two or three lines:

A cheque is a written instruction by an account holder to their bank to pay a specific amount to another person. It contains the payer’s name and signature, payee’s name, and a valid date. The amount is transferred from the payer’s bank account to the recipient’s account.

Guess the Words

1. The most popular instrument for money transfer is (//E///E)

Answer: C H E Q U E

2. Institutions where funds are kept safe (/A//K)

Answer: B A N K

3. RBI plays the role of what kind of bank in India (C///T//A/)

Answer: C E N T R A L

Abbreviations (Unit 3)

| Abbreviation | Full Form |

|---|---|

| BC | Before Christ |

| RBI | Reserve Bank of India |

| SBI | State Bank of India |

Unit 4 – Security and Modes of Digital Payments

4.1 Reserve Bank of India – Role and Importance

The RBI is the Central Bank of India with full power to control the monetary situation of the entire country.

Functions of RBI:

- Implements monetary policies

- Manages foreign exchange reserves

- Acts as banker to the government

- Provides financial regulation and supervision

- Governs the policies for other banks to follow

4.2 National Payments Corporation of India (NPCI)

- NPCI is the umbrella organisation for all retail payments in India.

- Incorporated in 2008 under guidance of RBI and Indian Banks’ Association (IBA).

- Provides infrastructure to the entire banking system for physical and electronic payment and settlement systems.

4.3 Introduction to Digital Banking

Digital banking allows bank customers to use banking services through the bank’s website on a laptop or through a mobile app on a smartphone or tablet.

Services available:

- Checking account balance

- Transferring funds to another account

- Ordering a cheque book

- Changing passcodes

Digital Banking – Do’s and Don’ts

| Do’s | Don’ts |

|---|---|

| Keep user ID and password confidential | Do not use email messages to log in |

| Memorise your password; do not write it down | Do not reveal personal information over email/SMS/phone |

| Log off completely and clear cache after every session | Do not save your banking password in browser |

| Register for SMS alerts to track transactions | – |

4.4 Understanding Digital Payments

Digital Payments means transferring money to another individual, business, or organisation through the internet without handling physical cash.

4.4.1 Benefits of Digital Payments

- No need to carry cash

- Transactions possible 24×7

- Fast and convenient

- Traceable and secure

- Useful for small and large amounts

4.4.2 Modes of Digital Payments – Card Based

Types of Banking Cards

| Card Type | How It Works | Key Feature |

|---|---|---|

| Debit Card | Deducts money directly from bank account | Dual purpose: ATM + purchases |

| Credit Card | Provides instant credit; pay back within ~1 month | Spend first, pay later |

| Prepaid Card | Pre-loaded with a specific amount | Spend only what is stored on the card |

Guidelines for Using Banking Cards

- Watch for people nearby when entering your ATM PIN.

- Pay credit card dues on time to avoid heavy interest charges.

- Keep cards safe; never let them go into wrong hands.

- Never share card PIN with anyone.

4.5 Various Channels for Acceptance of Card-Based Digital Payments

4.5.1 Point of Sale (PoS)

PoS is a system that automatically tracks each sale transaction and the amount received from the customer. It enables card-based transactions at shops and stores.

4.5.2 mPoS – Mobile Point of Sale

mPoS is a mobile phone-based application for merchants. It is easy to use and offers technological flexibility compared to traditional PoS machines.

4.5.3 Soft PoS

Soft PoS uses Tap-on-Phone technology. Merchants can accept payment from contactless cards directly on NFC-enabled Android mobile devices via a software-based payment app — no extra hardware is needed.

4.5.4 E-Commerce Payment

Purchasing goods and services online through an electronic medium without cash or cheques is called e-commerce payment.

Benefits:

- Security

- Efficiency

- Convenience

- User-friendliness

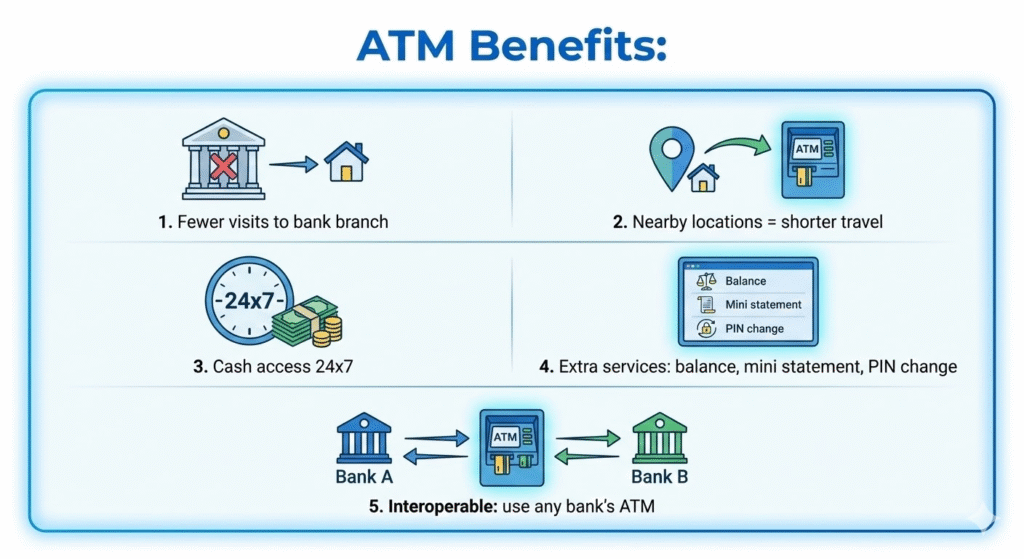

4.5.5 Automated Teller Machines (ATMs)

ATMs let bank account holders withdraw cash, check balance, and do other banking tasks without visiting the bank and at any time.

4.6 Modes of Digital Payments – Biometric Based

4.6.1 Unique Identification Authority of India (UIDAI)

- UIDAI was launched as a statutory authority in 2016.

- Its purpose: issue a unique identity document called Aadhaar (UID) to all citizens of India.

- Objective: eliminate duplicate and fake identities; enable easy individual authentication.

4.6.2 Aadhaar Enabled Payment System (AePS)

AePS is a payment system operated by NPCI. It allows Aadhaar-linked bank customers to perform basic banking through a business correspondent:

- Balance enquiry

- Cash deposit

- Cash withdrawal

- Mini statement

- Aadhaar-to-Aadhaar fund transfer

Authentication is done using the Aadhaar-linked fingerprint or iris scan.

4.6.3 Micro ATMs

Micro ATMs are handheld devices available with authorised banking correspondents (also called Bank Mitras). They allow Aadhaar holders to perform basic banking transactions in rural and remote areas.

- Authentication: Fingerprint and/or Retina/Iris scan.

- Portable: can be carried easily in one hand.

- Purpose: bring banking services to areas with no bank branches.

4.7 Modes of Digital Payments – Mobile Based Banking and Others

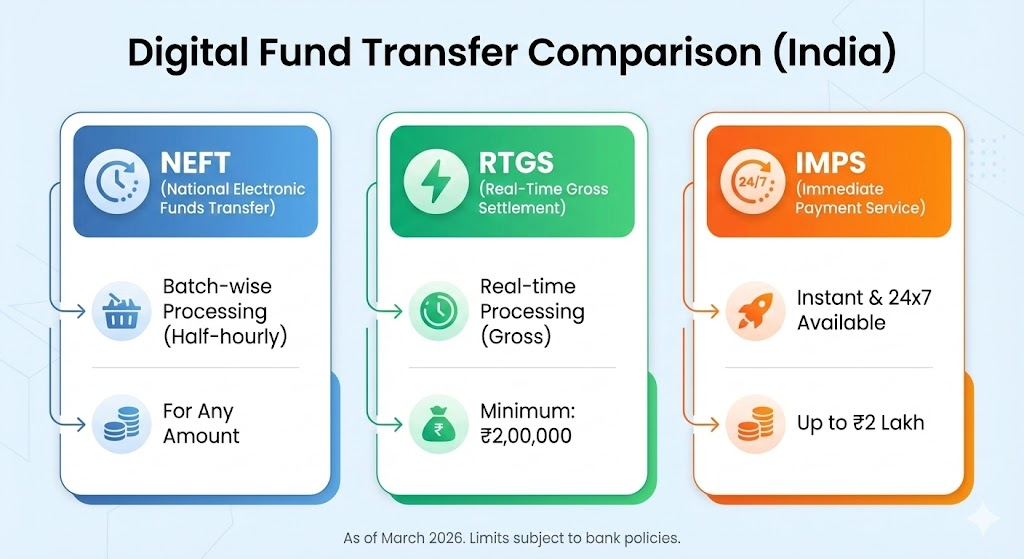

4.7.1 Internet Banking

Internet banking lets you manage your bank account over the internet using a laptop, tablet, or smartphone. Funds transfer can happen through:

| Method | Full Form | Key Features |

|---|---|---|

| NEFT | National Electronic Funds Transfer | Owned by RBI; nationwide; requires IFSC code |

| RTGS | Real-Time Gross Settlement | Real-time; for large values; minimum Rs.2,00,000; no upper limit; final and irrevocable |

| IMPS | Immediate Payment Service | By NPCI; 24×7; available on mobile, internet, ATM, SMS; limit Rs.2 lakh per transaction |

4.7.2 Mobile Banking – Bank in Your Pocket

Most banks offer a secure mobile banking app with these services:

- Checking account balance

- Making funds transfer

- Bill payments and card payments

- Service requests (cheque books, etc.)

Unified Payments Interface (UPI)

UPI is developed by NPCI and combines multiple bank accounts into one single mobile app.

- Enables seamless fund routing and merchant payments.

- Supports Peer to Peer collect requests.

- Works through QR codes.

How UPI QR Code Payment Works

Step 1: Customer scans UPI QR at merchant location

Step 2: Verifies UPI ID, amount, merchant name

Step 3: Enters UPI PIN

Step 4: Receives payment confirmation on UPI app + SMS

4.7.3 Mobile Wallets

A mobile wallet is a virtual wallet in a mobile app. It lets you make purchases by scanning a QR code at merchant establishments — even without carrying cash or cards.

Popular example in India: PayTM

4.7.4 Unstructured Supplementary Service Data (USSD)

USSD allows users without a smartphone or internet to access mobile banking using the code *99#.

- Works on basic feature phones.

- Objective: promote financial inclusion of underserved sections of society.

- Integrates people without smartphones into mainstream banking.

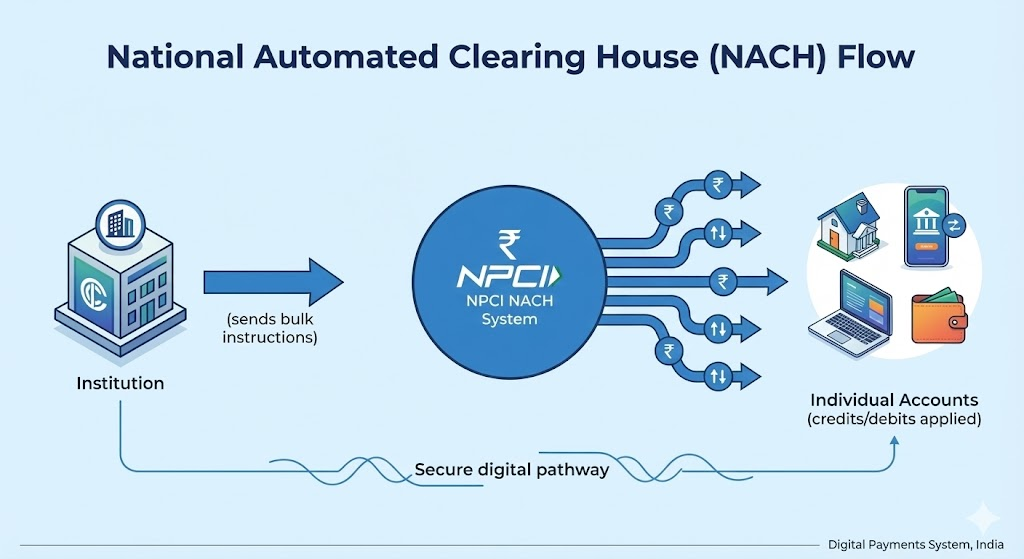

4.8 National Automated Clearing House (NACH)

NACH (earlier known as Electronic Clearing Service) is a service offered by NPCI to banks, financial institutions, corporates, and governments.

- NACH Debit: Automates recurring payments like EMIs, insurance premiums, utility bills.

- NACH Credit: Automates regular credits like salaries, subsidies, interest payments.

Unit 4 Questions with Answers

Choose the Correct Option

1. Which of the following contributes towards making online transactions secure?

a) Unique transaction ID b) Unique server ID c) Unique PC ID

Answer: a) Unique transaction ID

2. What is the name of the institution that governs policies for other banks to follow?

a) SBI b) RBI c) CBI

Answer: b) RBI

3. Choose the correct benefit of ATM:

a) Increased convenience b) Increased time taken c) Increased security risk

Answer: a) Increased convenience

4. Choose the correct full form of NEFT:

a) National Electrical Fund Transfer b) National Electronic Funds Transfer c) Nationwide Electronic Fund Transact

Answer: b) National Electronic Funds Transfer

True or False

1. RBI plays a prominent role and has the power to control the monetary situation of the entire country.

Answer: True

2. Digital payments are not easy and convenient.

Answer: False — Digital payments are easy, convenient, and available 24×7.

3. Debit cards serve a dual purpose.

Answer: True — They work at ATMs and for purchase transactions.

4. Card PIN numbers should be shared with friends and family.

Answer: False — PIN should never be shared with anyone.

5. QR codes make it easy and convenient to make payments through mobile wallets.

Answer: True

6. Micro ATMs are not portable and cannot be carried anywhere.

Answer: False — Micro ATMs are portable handheld devices.

Fill in the Blanks

1. Nowadays, most of the banks offer their customers the facility of __________ banking.

Answer: Digital

2. Digital payments can be made ________ of the day.

Answer: Anytime

3. Digital banking allows the bank customers to avail banking services using the bank’s website or a __________.

Answer: Mobile app

4. _______ is an innovative payment acceptance segment which uses ‘Tap-on-Phone’ technology.

Answer: Soft PoS

5. Purchase of goods and services online through an electronic medium without cash or cheques is known as _____________.

Answer: E-Commerce payment

Answer the Following

1. List any two Do’s and Don’ts of Digital Banking:

Do’s:

- Keep your user ID and password confidential.

- Log off completely and clear cache after every banking session.

Don’ts:

- Do not reveal personal information over email, SMS, or phone calls.

- Do not use the browser’s “Remember Password” feature for banking passwords.

2. Describe ATM and its purpose:

ATM stands for Automated Teller Machine. It is a machine that allows bank account holders to withdraw cash, check balance, and perform other banking tasks at any time without visiting the bank. ATMs are interoperable, meaning customers can use any bank’s ATM.

3. What is an mPoS?

mPoS (Mobile Point of Sale) is a mobile phone-based application designed for merchants to accept card-based digital payments. Unlike traditional PoS machines, mPoS is portable and has an easy-to-use interface, offering great technological flexibility.

Abbreviations (Unit 4)

| Abbreviation | Full Form |

|---|---|

| RBI | Reserve Bank of India |

| NPCI | National Payments Corporation of India |

| ATM | Automated Teller Machine |

| IMPS | Immediate Payment Service |

| UPI | Unified Payment Interface |

| USSD | Unstructured Supplementary Service Data |

| NACH | National Automated Clearing House |

| NEFT | National Electronic Funds Transfer |

| RTGS | Real-Time Gross Settlement |

| AePS | Aadhaar Enabled Payment System |

| UIDAI | Unique Identification Authority of India |

Download Mind Map

Visit our Class 6 Skill Development page for free mind maps of all Chapters