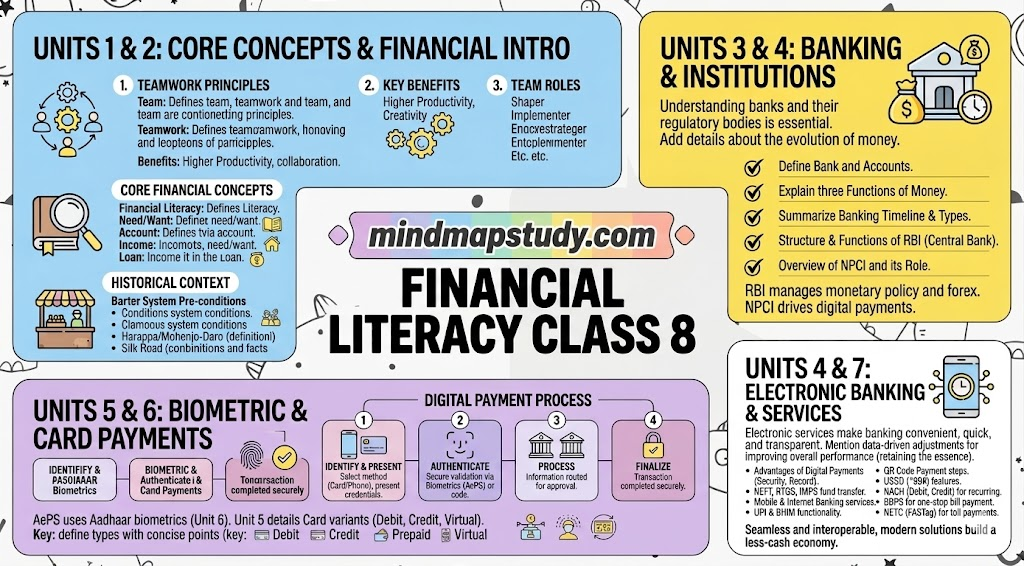

This CBSE handbook on Financial Literacy for Class 8 is a complete guide to money, banking, digital payments, and modern payment technologies — built by NPCI and published by CBSE. All seven units are covered here with clear notes, solved self-test questions, ASCII diagrams, and a full mind map ready for download.

Unit 1: Teamwork

1.1 Definition of Team

A team is a group of people who come together to perform individual tasks to achieve a common goal or objective. Each member contributes based on their own skills and competencies, making the combined output stronger than any individual effort.

1.2 Benefits of Teamwork

- Higher Productivity

- Better Cooperation

- Creativity and Problem Solving

- Sharing of Work

- Learning and Motivation

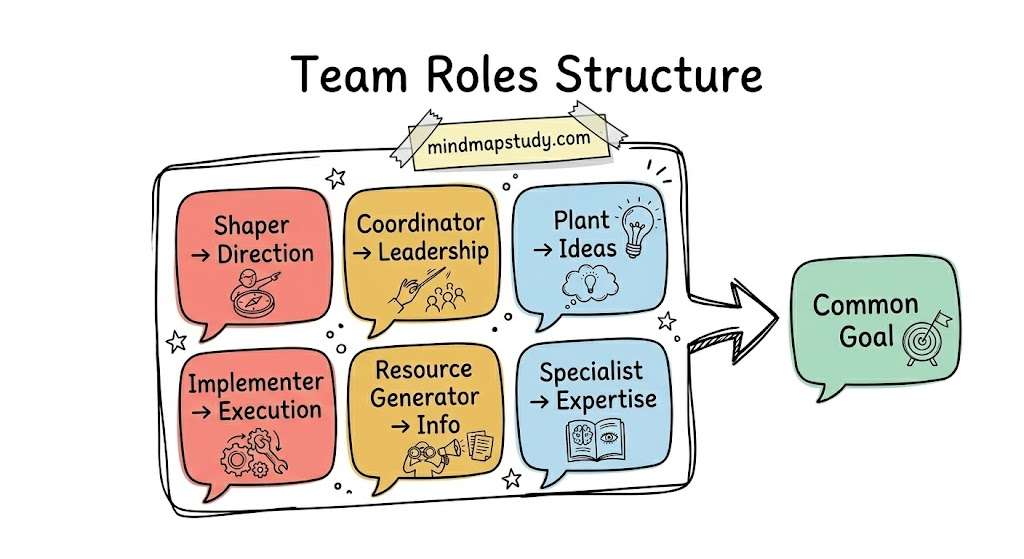

1.3 Team Roles

In Class 8, the focus is on understanding the specific roles team members play. Every member contributes differently based on their strengths:

| Role | Description |

|---|---|

| Shaper | Has a clear sense of direction; drives things forward |

| Implementer | Turns words into action; gets things done |

| Coordinator | Demonstrates leadership; manages group dynamics |

| Resource Generator | Gathers and provides necessary information for smooth working |

| Plant | Generates creative and random ideas; some may not be practical |

| Specialist | Demonstrates specialist knowledge and expertise |

Unit 1: Self-Test Questions – Solutions

Choose the correct option:

- Working in a team leads to:

- Answer: a. Increased Creativity

- An individual who demonstrates leadership skills in a team is known as:

- Answer: c. Coordinator

Answer in brief:

- List any two benefits of teamwork:

- Higher Productivity — team members work faster and more effectively together.

- Better Cooperation — members learn from each other’s mistakes and provide support.

- What is the difference between a Specialist and Resource Generator?

- A Specialist has deep knowledge or expertise in a particular field, which may or may not be directly useful to the team.

- A Resource Generator actively gathers and provides relevant information that keeps the team working smoothly.

Unit 2: Introduction to Financial Literacy

2. Introduction to Financial Literacy

Financial literacy is the possession of financial knowledge and skills that help a person make intelligent decisions about money. From managing pocket money to understanding bank accounts, being financially aware helps at every stage of life.

2.1 Needs and Wants

| Term | Meaning | Examples |

|---|---|---|

| Need | Necessary for survival and living standard | Wholesome food, comfortable clothing, shelter |

| Want | Desired for more satisfaction or enjoyment | Fancy car, lavish house, eating in restaurants |

2.2 Understanding Basic Financial Concepts

| Term | Meaning |

|---|---|

| Bank | A financial institution authorised by the Government to receive deposits and issue loans; also offers currency exchange, wealth management, and safe deposit boxes |

| Account | An accurate record of all transactions — both debit and credit — relating to an account holder |

| Income | Money that an individual or business earns by providing a good, service, or the use of assets |

| Loan | A sum of money offered as debt or advance, usually by a bank, on specific terms and charged with interest |

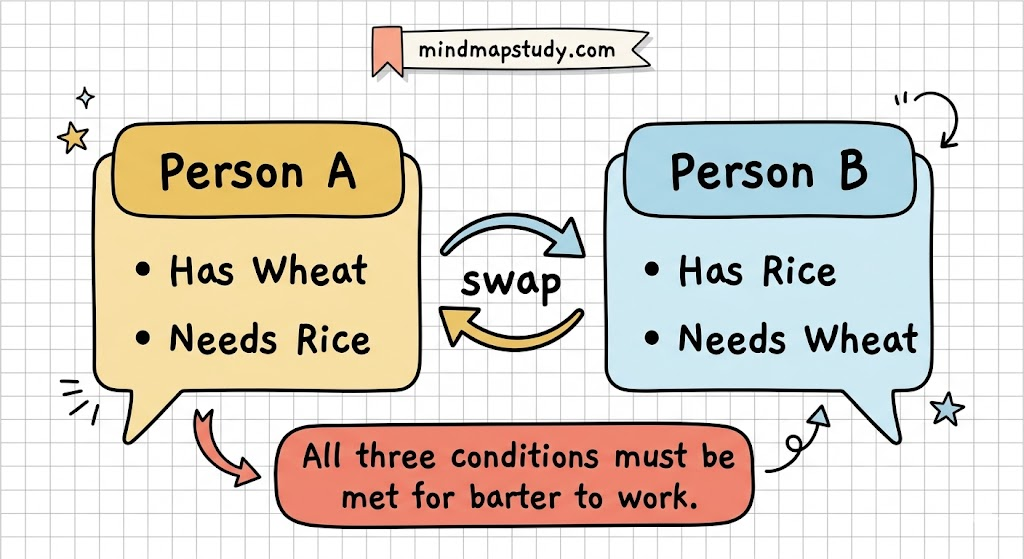

2.3 Barter System

Before money was developed, people traded goods using the Barter System — exchanging one product for another.

Three conditions for barter exchange to work:

- Person A must have a product that Person B needs, and vice versa.

- Both must be ready for the exchange at the same time.

- The products being exchanged must be of similar value.

2.3 Money and Trade

Money and trade are closely connected. Historically, even before money was invented, ancient civilisations like Harappa and Mohenjo-Daro had trade connections with Mesopotamia and traded in gold, silver, copper, gemstones, beads, pearls, sea shells, and terracotta pots.

The Han Dynasty (206 BC–220 AD) opened the famous Silk Road — the trade route between China and Central Asia — one of the oldest international trade routes in the world.

2.4 Bill/Cash Memos

Before formal banking existed in India, documents like Hundi and Chitti were used for business transactions and money transfers.

- Hundi was an instrument of exchange: an unconditional promise or order to pay money, capable of transfer by valid negotiation.

- As banking developed, people began depositing precious metals with lending individuals called Seths, who acted as bankers and provided funds to businesses.

A cash memo is a receipt issued in cash transactions. It serves as proof of the transaction for both the buyer and seller.

Unit 2: Self-Test Questions – Solutions

Choose the correct option:

- Which of the following has provided the key impetus to the development of trade across the world?

- Answer: b. Money

- “An accurate record of all transactions including debit and credit relating to an account holder” — this is called:

- Answer: a. Account

- A product necessary for your survival is known as:

- Answer: b. Need

Answer in brief:

- Describe the meaning of ‘Loan’ in your own words:

- A loan is a fixed sum of money borrowed from a bank or financial institution by a person, business, or government. The borrower agrees to repay the amount within a set period along with an additional charge called interest.

- What is the importance of cash memos in business?

- Cash memos serve as official proof of a cash sale transaction. They protect both the buyer and the seller from future disputes by documenting the items purchased, the quantity, the price, and the date of transaction.

True or False:

- Barter System has various limitations that led to the development of money. — True

- There is no evidence of trade having occurred in ancient India. — False (Harappa and Mohenjo-Daro had well-established trade with Mesopotamia.)

Unit 3: Banking

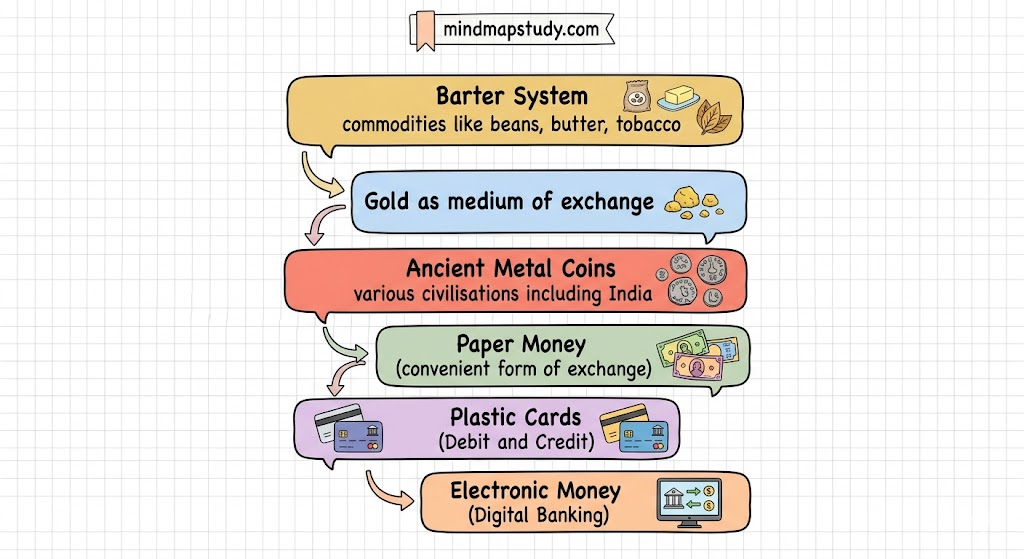

3.1 Evolution of Money

The evolution of money is closely linked to the growth of human civilisation, trade, and commerce. As business volumes grew, merchants needed a stable platform for transactions.

Money evolved in this order:

3.2 Importance of Money

Money serves three Imp functions:

| Function | Description | Example |

|---|---|---|

| Medium of Exchange | Accepted form of exchange in the market | Buying soap, paying school fees |

| Standard of Value | Defines the value of a product; categorises as high-priced or low-priced | Computers and cars are high-value; pencils are low-value |

| Store of Value | Can be kept safely for future use | Cash in wallet or deposits in bank |

3.3 Role of Banks

Banks enable money to function as a store of value by allowing storage and transaction through accounts. They also act as a secure platform for all business and economic transactions.

Banking in India started in a major way with the Imperial Bank of India in 1921, which was later renamed the State Bank of India (SBI) in 1955.

3.4 Types of Banks

| Type | Description | Examples |

|---|---|---|

| Central Bank | Most important institution; issues currency; manages monetary policy and foreign reserves | RBI |

| Public Sector Commercial Banks | Government-owned; also called nationalised banks | SBI, Canara Bank, Central Bank of India |

| Private Commercial Banks | Privately owned | ICICI Bank, HDFC Bank |

| Cooperative Banks | Promotes saving and investment in rural areas; funds agriculture, livestock, and self-employment | Various state cooperative banks |

| Specialised Banks | Support specific industries like foreign trade or industrial development | EXIM Bank, SIDBI, NABARD |

Imp RBI Functions:

- Issues currency notes.

- Manages foreign currency reserves.

- Controls money supply in the economy.

- Acts as custodian for reserve money.

- Checks and monitors all commercial bank activities.

Commercial Bank Services:

- Management of accounts

- Acceptance of deposits

- Lending of funds

- Cheque facilities for payments

- Online banking and phone banking

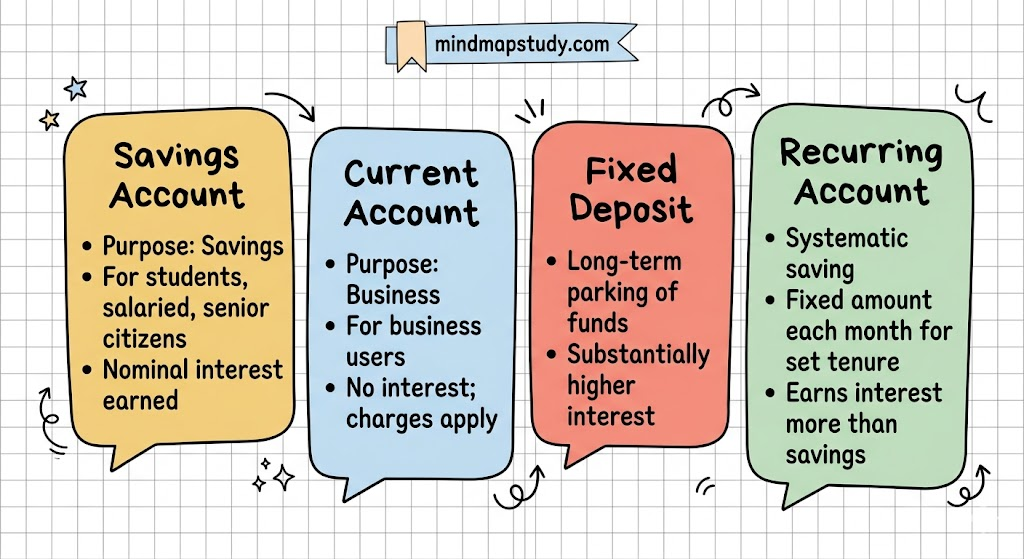

3.5 Types of Bank Accounts

Unit 3: Self-Test Questions – Solutions

Choose the correct option:

- Which is the oldest system of making business transactions?

- Answer: b. Barter System

- “Money helps us define the value of a product.” This relates to which function of money?

- Answer: b. Standard of Value

- This account is specifically targeted towards business owners:

- Answer: c. Current Account

True or False:

- Managing foreign currency reserves is among the key functions of RBI. — True

- Public sector commercial banks are owned by private entities. — False (They are owned by the Government.)

- One of the key functions of money is to act as ‘Store of Value’. — True

Answer in brief:

- Primary limitations of the Barter System:

- Both parties must have what the other needs at the same time.

- The products must be of similar value, which is hard to ensure.

- It becomes impractical for large-scale or long-distance trade.

- What are Specialised Banks?

- Specialised Banks are banks created to provide financial support to specific industry segments such as foreign trade or industrial development. Examples include EXIM Bank (for export-import), SIDBI (for small industries), and NABARD (for agriculture and rural development).

Unit 4: Security

4.1 Reserve Bank of India – Role and Importance

The Reserve Bank of India (RBI) is India’s central bank. It is led by the Governor, who is the chief executive. The Governor supervises and directs the affairs and business of the RBI, supported by Deputy Governors and Executive Directors.

At the top of RBI’s structure is the Central Board of Directors, which oversees the Reserve Bank and delegates specific functions to Local Boards and various committees.

4.1.1 Reserve Bank of India – Core Functions

- Monetary policy

- Regulation of banking and non-banking financial institutions

- Regulation of money, forex, and government securities

- Management of foreign currency reserves

- Banker to Banks

- Banker to the central and state governments

- Currency management

4.2 About NPCI

National Payments Corporation of India (NPCI) is a not-for-profit organisation that builds India’s retail payments and settlement infrastructure. It is an initiative of RBI and the Indian Banks’ Association (IBA).

NPCI’s shareholders include public sector banks, private banks, foreign banks, RRBs, cooperative banks, payments banks, payment system operators, and small finance banks.

4.3 Digital India Initiative

Digital India is a flagship programme of the Government of India with the vision to transform India into a digitally empowered society and knowledge economy. It is part of the larger Aatmanirbhar Bharat initiative.

Imp Digital India Initiatives:

| Initiative | Description |

|---|---|

| AePS | Bank-led model for online transactions at PoS/MicroATM using Aadhaar authentication |

| BHIM | App for simple, easy, quick payments using UPI |

| DigiLocker | Secure cloud platform for storing, sharing, and verifying important documents digitally |

| eBiz | Online portal for fast Government-to-Business (G2B) services |

| EPFO Web Portal | Allows employees to check EPF balance through an ePassbook |

4.4 Digital Payments

Digital payments allow banking customers to make instant payments without cheques — at any time of their convenience. The rapid expansion of high-speed internet and mobile technology has made digital payments widely accessible.

4.4.1 Advantages of Digital Payments

| Advantage | Description |

|---|---|

| Convenient | Available at any time, without specific banking hours |

| Easy and Quick | No cash or cheque handling; done through smartphones or computers |

| One-stop Solution | Transfer funds, buy goods/services, pay bills — all in one place |

| Accurate Record | Each transaction has a unique transaction ID; minimal risk; easy tracking |

| Transparent Transactions | Eliminates cash security risks; discourages use of black money |

Unit 4: Self-Test Questions – Solutions

Choose the correct option:

- Which of the following is NOT a function of RBI?

- Answer: c. Issuing cheques (RBI does not issue cheques; that is a commercial bank service.)

- The correct objective of Digital India initiative:

- Answer: a. Enhancing India’s digital economy

Fill in the blanks:

- RBI plays the role of being the banker to Government and Banks.

- Digital payments are backed with a unique record as each transaction generates a unique Transaction ID.

- Being transparent in their functioning, digital payments discourage the use of black money.

Unit 5: Modes of Digital Payments – Card Based

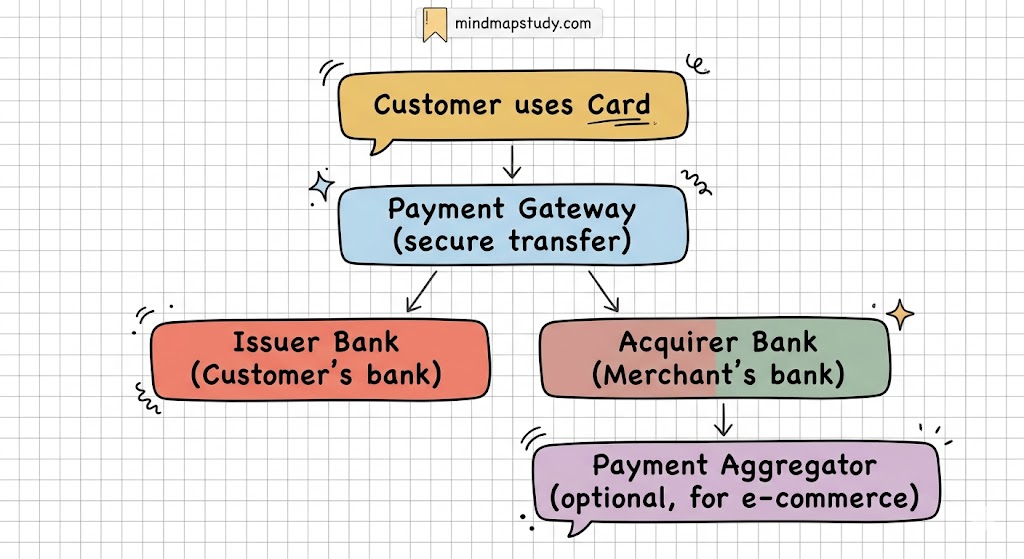

5.1 Payments Acceptance Ecosystem

| Component | Role | Example |

|---|---|---|

| Acquirer | Bank contracted with merchants; installs PoS | SBI Merchant Services |

| Issuer | Bank that issues debit/credit cards to customers | HDFC Bank |

| Payment Gateway | Securely transfers information between customer, merchant, and bank | Secure server link |

| Payment Aggregator | Enables e-commerce merchants to accept multiple payment modes without a separate bank account | Razorpay, PayPal, PayTM |

5.2 Use of Banking Cards

5.2.1 Types of Banking Cards

| Card Type | How It Works | Best For |

|---|---|---|

| Debit Card | Amount deducted directly from bank account | ATM + cashless merchant payments |

| Credit Card | Bank provides credit; 30–45 days to repay; interest on delayed payment | Convenience shopping |

| Prepaid Card | Stored value card charged with a fixed amount; more value added when exhausted | Meal cards, salary cards, gift cards |

| Virtual Card | One-time, non-physical card; expires after single transaction | Safe online transactions |

| Co-branded Card | Bank + retailer collaboration; reward points/cashback on purchases | Petrol cards, store loyalty cards |

| Contactless Card | Tap-on-machine payment; no PIN required for small amounts; RuPay contactless aligns with NCMC | Metro, bus, cab payments |

5.2.2 Guidelines for Use of Banking Cards

- Be alert at ATMs — ensure no one can see your PIN entry.

- Pay credit card dues on time to avoid heavy interest charges.

- Keep banking cards safe and out of wrong hands.

- Never share Card PIN or CVV numbers with anyone.

5.2.3 Activation of Banking Cards

- Controlled by the central computer system of the issuing bank.

- A card works only when set to active state by the bank on confirmation from the user.

- New cards are activated after the bank confirms the card is with the authorised person.

- Activation possible via: Internet Banking, Mobile Banking, Phone Banking, or ATM of the issuing bank.

- Each card has a valid till date — it is automatically deactivated beyond this date.

5.2.4 Do’s and Don’ts while Using Banking Cards

| Do’s | Don’ts |

|---|---|

| Keep banking cards in a safe and secure place | Do not delay informing the bank if the card is lost or stolen |

| Keep the card secure with a non-obvious PIN | Do not share PIN, CVV, card number, or expiry date with anyone |

| Clear credit card dues on time | Do not use credit card for extravagance; use it for convenience only |

5.3 Various Channels for Acceptance of Card Based Digital Payments

5.3.1 Point of Sale (PoS)

PoS replaces paper-based invoicing with automatic machine-based invoicing and inventory management.

PoS Benefits to Merchants:

- Faster Process: Improves customer service levels and saves time.

- Inventory Management: Automatic, professional stock tracking.

- Sales Report: Easy and instant report generation for tracking income and profits.

- Improved Customer Satisfaction: Faster, efficient shopping experience.

PoS Benefits to Customers:

- Faster billing — automated, no manual errors.

- Better accuracy — minimal incorrect billing.

- Improved shopping experience — fast, convenient, hassle-free.

Types of PoS systems:

- Counter-based PoS

- Mobile PoS (mPoS)

- Online PoS – e-commerce

- Omni-channel PoS

5.3.2 mPoS – Mobile Point of Sale

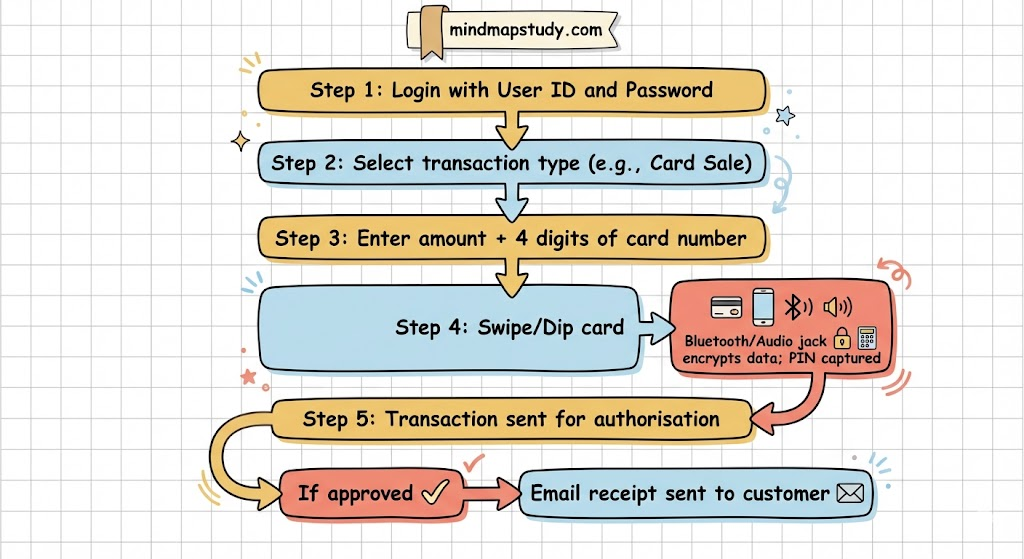

mPoS is a Java/iOS mobile application for merchants. When the card is swiped, data is encrypted and sent to the server for authentication.

How mPoS works:

5.3.3 Soft PoS

Soft PoS uses Tap-on-Phone (NFC) technology. Merchants accept contactless card payments directly on an NFC-enabled Android phone — no extra hardware needed. This makes the product affordable and enables wider market reach.

5.3.4 E-commerce Payment

An online PoS system used for internet-based transactions through net banking or banking cards. India’s e-commerce industry is a multi-billion dollar industry with a vast customer base.

5.3.5 Automated Teller Machine (ATM)

ATMs reduce bank branch crowd and give customers a one-stop solution for cash withdrawal, balance enquiry, mini statements, and more — 24×7.

ATM Benefits to Banks:

- Customer satisfaction — 24×7 access to banking services.

- Reduces crowding at branches.

- Enhances customer loyalty.

- Interoperability — customers can use any bank’s ATM.

ATM Benefits to Customers:

- Fewer visits to bank branch.

- Shorter travel time.

- Convenient 24×7 cash access.

- Balance enquiry, mini statement, PIN change.

- Interoperable — any bank’s ATM can be used.

Types of ATM Deployments:

| Feature | White Label ATMs (WLA) | Brown Label ATMs (BLA) |

|---|---|---|

| Ownership | Non-banking financial institutions (authorised by RBI) | Hardware owned by service provider |

| Branding | No specific bank branding; some carry WLA + partner logo | Carries sponsor bank’s logo |

| Cash | Provided by sponsor bank | Provided by sponsor bank |

| Common in | Smaller and remote towns | Regular locations |

Additional types:

- Onsite ATMs — located at bank branches.

- Offsite ATMs — located away from bank branches.

- Cash Deposit Machines (CDM) — deposit cash without filling a slip or queuing.

- Cash Recyclers — same as ATM plus cash deposit facility; reduces cash handling costs.

5.4 RuPay Network and RuPay Card

RuPay is India’s own domestic card payment network, created by NPCI. Its name comes from Rupee + Payment. It is a highly secure network that protects against phishing and enables a less-cash economy as per RBI’s vision.

RuPay Card Variants:

- RuPay Classic

- RuPay Platinum

- RuPay Select

- RuPay Corporate

The RuPay Contactless card aligns with the National Common Mobility Card (NCMC) program and works across metros, buses, and cabs, enabling an Interoperable Fare Management System (IFMS).

Unit 5: Self-Test Questions – Solutions

Choose the correct option:

- Which kind of banking card works on the basis of a pre-filled amount?

- Answer: c. Prepaid Card

- The interest paid on a credit card depends on?

- Answer: c. Credit period

- Which is a valid benefit of PoS to customers?

- Answer: b. Accuracy and convenience

- The kind of ATM that works on cost/revenue sharing basis:

- Answer: c. Brown Label ATM

- Which machine allows the facility to deposit cash?

- Answer: a. CDM (Cash Deposit Machine)

True or False:

- Debit cards are usually issued at the time of bank account opening. — True

- For purchases on a credit card, the amount is directly deducted from the account. — False (It is provided as credit; the account is not immediately debited.)

- ATMs are always located within the bank branch. — False (Offsite ATMs are located away from bank branches.)

Fill in the blanks:

- PoS system provides automatic machine-based invoicing and inventory record management.

- White Label ATMs are owned and operated by Non-banking financial Institutions authorised by RBI.

- mPoS system is based on Java/iOS application.

- Payment Aggregator is a service provider that registers and enables e-commerce merchants to accept various payment modes.

Unit 6: Modes of Digital Payments – Biometric Based

6.1 Unique Identification Authority of India (UIDAI)

UIDAI was established under the Aadhaar Act 2016 on 12 July 2016 by the Government of India. Its objective is to issue unique identity documents called Aadhaar (UID) to all residents of India.

The first UID number was issued on 29 September 2010 to a resident of Nandurbar, Maharashtra.

The UID is designed to be:

- Robust enough to eliminate duplicate and fake identities.

- Verifiable and authenticable in an easy, cost-effective way.

6.2 Aadhaar Enabled Payment System (AePS)

AePS is operated by NPCI. It uses Aadhaar biometric authentication to allow basic banking transactions, especially for financial inclusion in remote India.

To perform AePS transactions, the customer:

- Enters Aadhaar number.

- Selects bank name from drop-down on Micro ATM.

- Selects the type of service required.

- Provides biometric (fingerprint or iris) for authentication.

6.2.1 AePS Features

Financial Transactions:

- Balance Enquiry

- Cash Withdrawal

- Cash Deposit

- Fund Transfer

- Mini Statement

- BHIM Aadhaar

Non-Financial Transactions:

- Best Finger Detection

- Electronic Know Your Customer (eKYC)

- Demographic Authentication

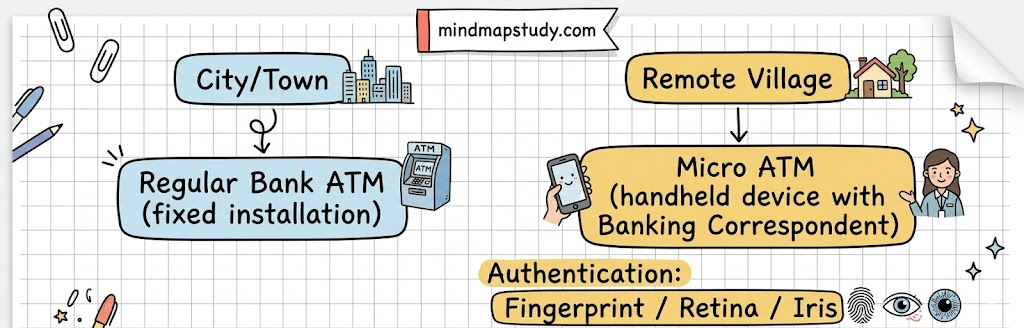

6.3 Micro ATMs – A Perfect Solution for Rural and Hinterlands

Regular ATMs are not available in far-flung rural areas — sometimes even a bank branch is absent. Micro ATMs are the solution.

Micro ATM Benefits:

- Low cost and portable — can be carried anywhere in one hand.

- Easy to set up in remote areas.

- Biometric-enabled secured transactions.

- Interoperable — works for any bank.

- Can be made compatible with regional languages.

- Fraction of the cost of a conventional ATM.

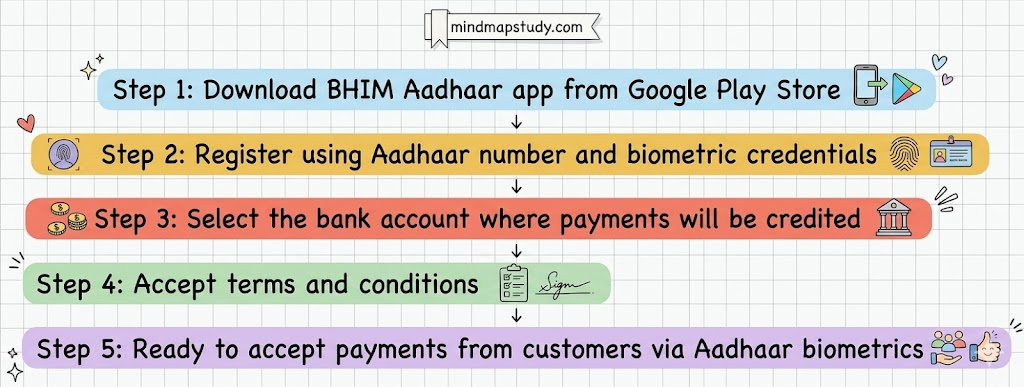

6.4 BHIM Aadhaar Pay – The Merchant Solution

BHIM Aadhaar Pay lets merchants accept digital payments from customers using Aadhaar biometrics — no card needed.

Merchant requirements:

- Android mobile with BHIM Aadhaar app.

- Certified biometric scanner connected to PoS/mPoS/Micro ATM via USB.

Customer requirement:

- Aadhaar linked to bank account.

Steps for First Time BHIM Aadhaar Pay Merchant Registration:

Unit 6: Self-Test Questions – Solutions

Choose the correct option:

- Institution created to issue unique identity to all citizens:

- Answer: c. UIDAI

- For BHIM Aadhaar Pay to work, Aadhaar must be linked to bank account for:

- Answer: a. Only Customer (The merchant registers separately with credentials; the customer’s Aadhaar must be bank-linked.)

- Which feature of Micro ATMs makes them more suitable for remote locations?

- Answer: c. Portable

True or False:

- UIDAI is a Government institution that aims to make digital financial transactions transparent. — False (UIDAI’s primary objective is unique identity; transparency in transactions is a result, not the stated primary aim.)

- BHIM app is not available on Google Play Store. — False (BHIM is available on both Google Play Store and Apple App Store.)

- Micro ATMs are portable and hand-held devices. — True

Unit 7: Modes of Digital Payments – Mobile Based Banking and Others

7.1 Internet Banking

Internet banking allows financial transactions over the internet using a smartphone, tablet, or laptop. The key advantage is that account holders can transfer funds to a beneficiary at any time of their convenience without using cheques.

Internet banking transfer methods:

| Method | Full Form | Operated By | Transfer Limit | Imp Feature |

|---|---|---|---|---|

| NEFT | National Electronic Fund Transfer | RBI | No fixed limit | Half-hourly batch processing; pan-India coverage |

| RTGS | Real-Time Gross Settlement | RBI | Min ₹2,00,000; no upper limit | Real-time, final, irrevocable; large value transfers |

| IMPS | Immediate Payment Service | RBI + NPCI | Min ₹1; Max ₹2 lakh per transaction | 24×7 instant; works on Mobile, Internet, ATM, SMS |

7.1.1 National Electronic Fund Transfer (NEFT)

NEFT is a nationwide centralised payment system owned and operated by RBI. Before making an NEFT transfer, the account holder must register the beneficiary’s account details: name, account type, account number, and IFSC code (Indian Financial System Code — an 11-digit code identifying individual bank branches).

Imp advantages of NEFT:

- Available round the clock, all days of the year.

- Near-real-time funds transfer.

- Secure settlement process.

- Pan-India coverage through a large network of bank branches.

- Positive confirmation to the remitter by SMS/email on credit.

7.1.2 Real-Time Gross Settlement (RTGS)

RTGS processes money transfers in real time — instructions are executed the moment they are received. Gross Settlement means each transfer is settled individually. All RTGS payments are final and irrevocable.

RTGS is meant primarily for large value transactions: minimum ₹2,00,000 with no upper limit.

Imp advantages of RTGS:

- Safe and secure.

- No cap on maximum transfer amount.

- Available 24x7x365.

- Real-time transfer of funds.

7.1.3 Immediate Payment Service (IMPS)

IMPS offers 24×7 instant fund transfer accessible on multiple channels — Mobile, Internet, ATM, and SMS. Funds can be sent using just the beneficiary’s mobile number and MMID (Mobile Money Identifier) — no bank account number needed.

Imp advantages of IMPS:

- Fast, safe, and secure.

- Works on net banking and mobile platforms; available on holidays too.

- Transfer confirmation sent to both payer and payee.

- Fund transfer limit: ₹2 lakh per transaction; minimum: ₹1.

7.2 Mobile Banking – Bank in Your Pocket

Mobile banking refers to making financial transactions on a mobile device — smartphone or tablet.

Services available through Mobile Banking:

- Checking account balance

- Making funds transfer

- Bill payments and card payments

- Service requests (cheque books, etc.)

- Locating branches and nearby ATMs

- Opening or closing an account

- Checking transaction history

7.2.1 Advantages of Mobile Banking

- 24x7x365 access to banking services.

- Saves time and money by avoiding physical branch visits.

- Better control over account and finances.

- Reduces paperwork through digital technology.

7.2.2 Do’s and Don’ts while Using Mobile Banking

| Do’s | Don’ts |

|---|---|

| Use only the bank-authorised mobile banking app | Do not fall prey to fake apps that steal user identity |

| Keep a strong password/PIN | Do not share PIN or OTP with anyone |

| Keep your mobile free from malware | Do not install apps from non-secure sources |

7.3 Unified Payments Interface (UPI)

UPI, developed by NPCI, combines the power of multiple bank accounts into a single mobile app. A UPI ID is a unique payment address — just like an email address — used to send or receive money. Example: abcd@upi

7.3.1 Imp Features of UPI

- Easy, safe, and instant transactions.

- Access multiple bank accounts from one app.

- Send/receive money across 200 banks and 21 third-party apps.

- Direct bank payments using UPI ID or UPI QR.

- Single-click authentication using UPI PIN.

- Payments for daily expenses, e-commerce, bills, and more.

7.3.2 UPI Benefits

| Beneficiary | Benefits |

|---|---|

| Banks | Single-click two-factor authentication; universal transactions; leverages existing infrastructure; safer and innovative |

| Customers | Single app for multiple accounts; use of Virtual ID (no credential sharing); single-click authentication; raise complaints directly from app |

| Merchants | Seamless fund collection using single identifier; no risk of storing card data; tap customers without cards; suitable for e-commerce and in-app payments |

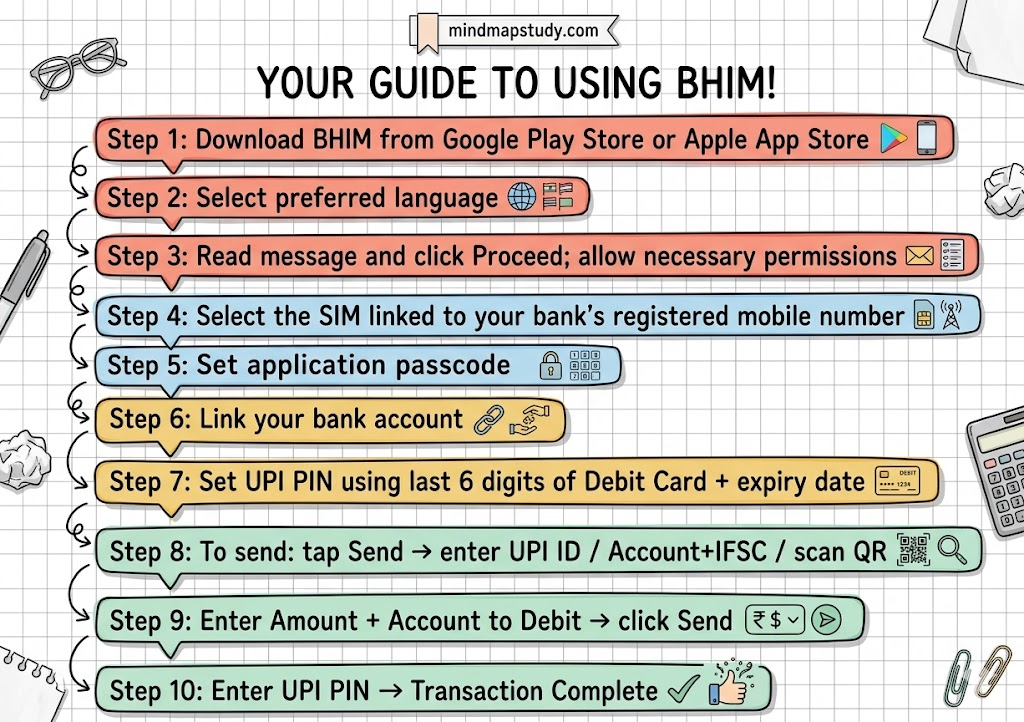

7.4 Bharat Interface for Money (BHIM)

BHIM is a digital payments app created by NPCI for simple, safe, and quick bank-to-bank payments using UPI.

Imp features of BHIM:

- Send Money: Via UPI ID, Account number/IFSC, or QR Scan.

- Request Money: Collect funds via UPI ID; also transfer via mobile number or Account/IFSC.

- Scan and Pay: Scan QR code at any merchant showing BHIM UPI or Bharat QR logo.

- Transactions: Check transaction history; filter and get mini statements.

- Language: Available in 20 languages including Hindi, English, Tamil, Telugu, Malayalam, Bengali, Gujarati, Marathi, and more.

7.4.1 Steps for First Time BHIM User

Important: Never share your OTP, Debit card details, or UPI PIN with anyone.

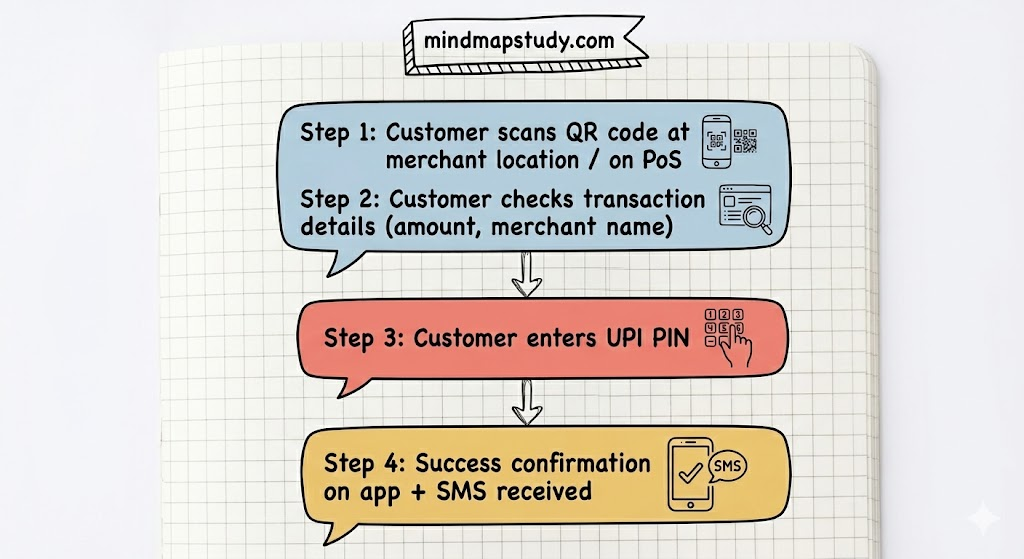

7.5 QR Codes – An Easy Way to Pay

QR (Quick Response) codes make UPI payments fast and simple.

7.6 Mobile Wallets – The Smart Way to Make Payments

A mobile wallet is a virtual wallet app that allows purchases by scanning the QR code at a merchant. A popular example is PayTM.

Mobile wallets store your credit or debit card information so payments are hassle-free.

Imp benefits of mobile wallets:

- Make payments without cash or cards.

- Pay utility bills conveniently.

- Fast transactions with instant confirmation.

- Secure, authenticated platforms.

- Cashbacks and reward points.

7.7 Unstructured Supplementary Service Data (USSD)

USSD is for people who do not have smartphones or internet access. Using the code *99# on any basic mobile phone, users can access mobile banking services.

USSD is available in 12 languages including English, Hindi, Tamil, Bengali, and Kannada.

7.7.1 USSD – Imp Services

- Checking account balance

- Generating account statements

- Making fund transfers

7.7.2 USSD Benefits

- Works on all phones — feature phone or smartphone.

- No internet or data connection needed; works on signalling channel.

- Round-the-clock availability.

7.8 Other Modes of Payment

7.8.1 National Automated Clearing House (NACH)

NACH is an electronic funds transfer system by NPCI for regular, recurring transactions.

Three types of NACH:

| Type | How It Works | Example |

|---|---|---|

| NACH Debit | Fixed amount deducted from account monthly | Loan EMI, mutual fund investment |

| NACH Credit | Fixed amount credited regularly | Monthly salary to employees |

| APBS (Aadhaar Payments Bridge System) | Aadhaar number becomes the financial address; government subsidies transferred directly to beneficiaries | Direct Benefit Transfer (DBT) subsidies |

Imp advantages of NACH:

- Creates a regular payment framework; improves customer relationships.

- Reduces paper use; encourages online transactions.

- Reduces risk of delayed payments.

- Useful for insurance premiums, loan instalments, credit card payments, mutual funds.

- Enables government subsidy distribution to beneficiary accounts.

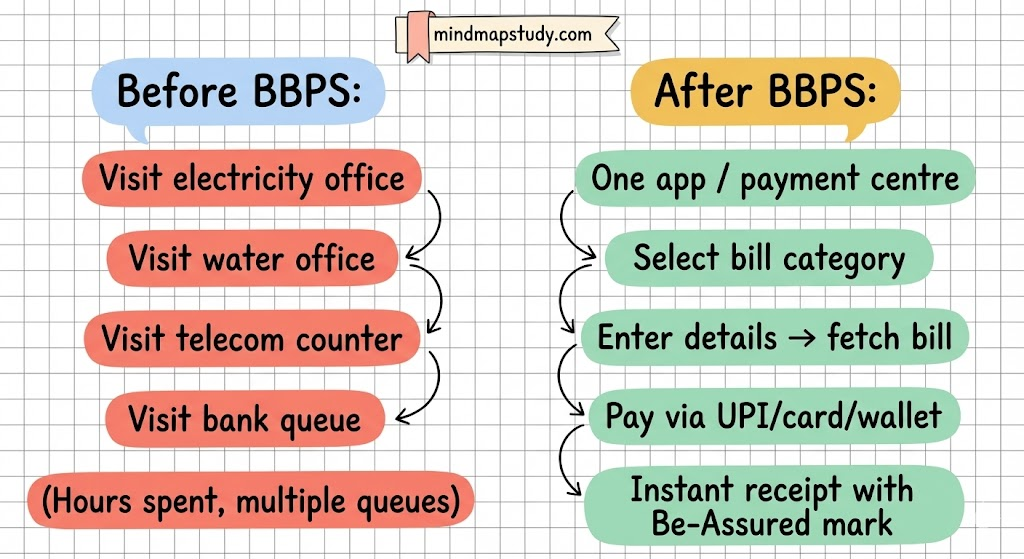

7.8.2 Bharat Bill Payment System (BBPS)

BBPS was conceptualised by RBI and implemented by NPCI. It is a one-stop ecosystem for payment of all bills, accessible 24×7 across India.

BBPS Customer Workflow:

- Visit preferred banking app/website or any BBPS-enabled kirana shop.

- Select the bill category (electricity, gas, water, telecom, etc.).

- Enter basic details (mobile number, customer ID) to fetch bill.

- Select payment mode — UPI, net banking, card, wallet.

- Account gets debited; customer receives a successful receipt with Be-Assured mark.

7.8.3 National Electronic Toll Collection (NETC)

NETC uses FASTag — a device using Radio Frequency Identification (RFID) technology — to make toll payments directly from the customer’s linked account while the vehicle is in motion.

NETC was launched by the Government of India along with NPCI.

Objectives of NETC:

- Electronification of retail payments.

- Lowering air pollution by reducing congestion at toll plazas.

- Reduction of fuel consumption.

Imp Features of FASTag:

- Interoperability: FASTag issued by any member bank is accepted at all NETC-covered toll plazas.

- Flexibility: Link FASTag to savings, current, or prepaid account; no existing bank relationship mandatory for prepaid accounts.

- Cashless Payment: Payments made while vehicle is in motion.

- Save Time and Fuel: No stopping at toll plaza; reduces congestion.

Unit 7: Self-Test Questions – Solutions

Choose the correct option:

- Which internet banking option allows 24×7 instant fund transfer on multiple channels?

- Answer: c. IMPS

- What makes UPI-based payments extremely easy and convenient?

- Answer: a. QR Codes

- Which is an example of a mobile wallet?

- Answer: a. PayTM

Mention the full forms:

- RTGS — Real-Time Gross Settlement

- IMPS — Immediate Payment Service

- IFSC — Indian Financial System Code

- NACH — National Automated Clearing House

- USSD — Unstructured Supplementary Service Data

Answer the following:

- Advantages of NEFT:

- Available round the clock, all days of the year.

- Near-real-time funds transfer to beneficiary account.

- Secure settlement process.

- Pan-India coverage via a large network of bank branches.

- Positive confirmation by SMS/email on credit to beneficiary account.

- Vital services provided by Mobile Banking:

- Checking account balance.

- Making funds transfer.

- Bill payments and card payments.

- Service requests such as ordering cheque books.

- Locating branches and nearby ATMs.

- Opening or closing an account.

- Checking transaction history.

- What is UPI?

- UPI (Unified Payments Interface) is a system developed by NPCI that combines multiple bank accounts into one mobile app. It uses a unique UPI ID — like an email address — to send and receive money instantly. It works across 200 banks, supports multiple payment channels, and uses a single-click UPI PIN for authentication.

- NACH types (3):

- NACH Debit: Fixed amount deducted monthly — used for loan EMIs, mutual fund payments.

- NACH Credit: Fixed amount credited monthly — used for salary payments to employees.

- APBS (Aadhaar Payments Bridge System): Aadhaar number used as financial address for direct subsidy transfer by the Government.

- Imp benefits of mobile wallets:

- Make payments using mobile without cash or cards.

- Pay utility bills conveniently.

- Transactions are fast with instant confirmation.

- Secure platforms based on authenticated users.

- Benefits like cashbacks and reward points.

Download Free Mind Map from the link below

This mind map contains all important topics of this chapter